- Home

- Credit Score

- Check HDFC Bank CIBIL Score

HDFC Bank CIBIL Score: How to Check and Improve Your HDFC CIBIL Score

The Credit Information Bureau India’s CIBIL Score is an important metric in India’s financial landscape that acts as a financial report card, summarising an individual’s creditworthiness. Ranging from 300 to 900, this three-digit score reflects a person’s credit history and repayment behavior, playing a crucial role in their eligibility for various financial products, including credit cards, personal loans, and home loans. HDFC Bank, a leading name in the Indian private banking sector.

- Instant Results

- No Hidden Fees

- Secure & Confidential

- No Impact on Your Credit Report

I agree to the Terms and Conditions of TUCIBIL and hereby provide explicit consent to share my Credit Information with Urban Money Private Limited.

Verify your number

Enter 6 Digit OTP

Change mobile number

Table of Content

How to Check Your HDFC CIBIL Score?

Awareness of the HDFC CIBIL score is important for responsible financial management. HDFC Bank, in collaboration with CIBIL, offers convenient methods for customers to check their scores. Here is a step-by-step guide:

- Visit the official CIBIL website (www.CIBIL.com).

- Locate the “Get Your CIBIL Score” section.

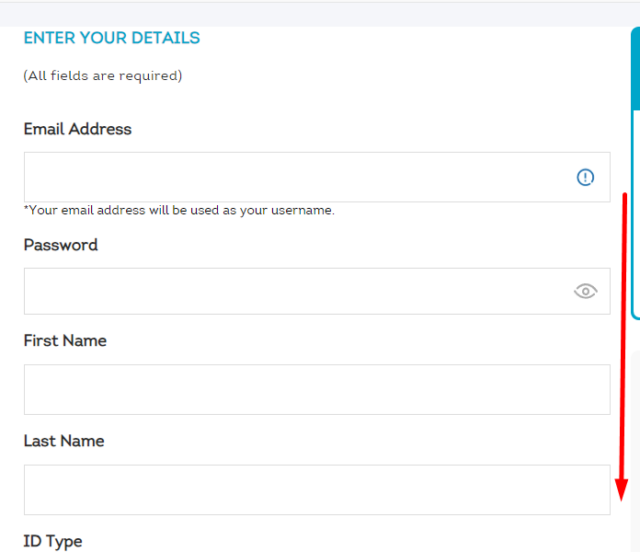

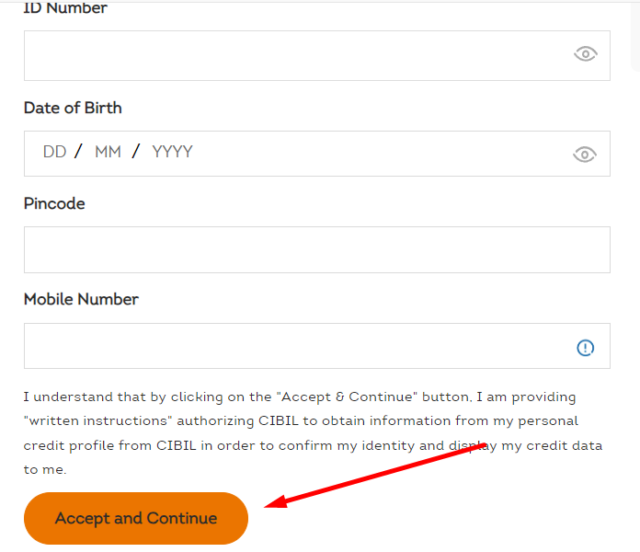

- Fill out the online application form with your personal details, including your full name, date of birth, and PAN number.

- Answer questions about your credit history, such as the number of credit cards you possess and any loans you have taken.

- Submit the form and pay the nominal fee associated with the credit report.

Upon successful submission, you will receive your CIBIL Score report, which details your credit history, repayment behaviour, and factors influencing your score. Regularly monitoring your CIBIL Score allows you to identify potential issues and take corrective actions to improve it.

Role of CIBIL Score in Securing an HDFC Bank Credit Card

Obtaining an HDFC Bank credit card necessitates meeting specific HDFC CIBIL score requirements. Generally, a score closer to 900 is considered excellent, significantly increasing the likelihood of credit card approval. However, a score of 750 or above is often considered the minimum threshold for HDFC Bank credit cards. This score assures the bank of the applicant’s responsible credit management and reduces the risk associated with lending. While individuals with scores below 750 may still be eligible for certain cards, they might face higher interest rates, lower credit limits, or stricter eligibility criteria. It is important to note that the specific score requirement can vary depending on the type of HDFC Bank credit card being applied for. Premium cards with exclusive benefits often require a higher CIBIL Score than standard cards. Additionally, certain specialised cards for students or individuals with limited credit history may have slightly lower score requirements. Maintaining a good CIBIL Score is crucial for securing favourable terms and conditions on any HDFC Bank credit card, maximising the benefits and minimising potential downsides associated with credit card usage.

Eligibility Criteria for HDFC Bank Credit Cards

Beyond the HDFC CIBIL score, additional eligibility criteria must be met to qualify for an HDFC Bank credit card. These factors include:

- Residency: Applicants must be Indian residents.

- Age: The minimum age requirement typically ranges between 21 and 25, depending on the specific card. The upper age limit is usually 65.

- Income Stability: A stable income source with a minimum threshold based on the card type is mandatory. Income documents like salary slips or income tax returns are required for verification.

- Employment Status: Salaried individuals, self-employed professionals, and individuals with agricultural income may be eligible, depending on the card and their income stability.

Factors Affecting HDFC CIBIL Score

Several factors influence the HDFC CIBIL score; here are some key elements:

- Repayment History: Timely payments of EMIs, credit card bills, and other loans significantly improve the CIBIL Score. On the other hand, late payments, defaults, or write-offs negatively impact your score.

- Credit Utilisation Ratio: This ratio refers to the amount of credit you use compared to your credit limit. Ideally, maintaining a utilisation ratio below 30% demonstrates responsible credit management and positively impacts your score.

- A mix of Secured and Unsecured Loans: A healthy mix of secured loans, such as home loans, and unsecured loans, like credit cards, indicates responsible credit behaviour and can improve your score.

- Length of Credit History: A longer credit history with a consistent track record of on-time payments strengthens the CIBIL Score. On the other hand, a limited credit history or no credit history can make obtaining a high score challenging.

- Hard Inquiries: Every time you apply for a new loan or credit card, a “hard inquiry” is registered on your credit report, which can slightly lower your score. Limiting frequent applications can help maintain a good score.

Range Table for HDFC CIBIL Score

Here is the range table for HDFC CIBIL scores for a quick reference. This table categorises credit scores used by HDFC and other financial institutions. A higher CIBIL Score indicates better creditworthiness, which can be beneficial when applying for loans or credit cards.

| CIBIL Score Range | Credit Quality |

| 300 – 549 | Poor Credit |

| 550 – 649 | Fair Credit |

| 650 – 699 | Good Credit |

| 700 – 749 | Very Good Credit |

| 750 – 900 | Excellent Credit |

How Can the Low Credit Score of HDFC Bank be Improved?

A low HDFC CIBIL score is not an irreversible situation. By adopting responsible financial practices, you can improve your score over time and increase your chances of obtaining an HDFC Bank credit card. Here are some effective strategies:

- Make Timely Payments: Ensure on-time payments for all your EMIs, credit card bills, and other loans. Even a single missed payment can significantly damage your score.

- Maintain Low Credit Utilisation: Keep your credit card balances low and avoid exceeding your credit limit. Ideally, aim for a utilisation ratio below 30%.

- Build a Positive Credit History: If you have a limited credit history, consider obtaining a secured loan, like a small personal loan and repaying it diligently. This demonstrates responsible credit management.

- Dispute Errors: Regularly review your CIBIL report for any inaccuracies and promptly initiate a dispute resolution process if you find any errors.

- Avoid Frequent Loan Applications: Limit your application for new loans or credit cards to a short period. Each application triggers a hard inquiry that can temporarily lower your score.

By following these tips and maintaining disciplined financial behaviour, you can gradually improve your HDFC CIBIL score and enhance your eligibility for HDFC Bank credit cards, unlocking a wider range of financial products and opportunities.

Last Updated: 28th April 2025

Latest from the Credit Score Blog

Get in-depth knowledge about all things related to Credit Score and your finances

CIBIL Score for Mudra Loan

Is CIBIL score required for Mudra loan? Search for the Mudra loan CIBIL score online, and you’ll probably come away more confused than informed. One website claims you need a score of 650. Another pushes the figure to 70

CIBIL Score for Women Housewives and Homemakers

Why is a CIBIL score equally important for women? The credit score has become an essential factor for most lending decisions. It is used by banks and NBFCs to analyze a person’s previous experience in managing credit. Fo

Credit Score vs CIBIL Score

What is a credit score? A credit score is nothing but a three-digit number that shows how well you have been handling borrowed funds. It is generated from data such as loan repayments, credit card transactions, outstandi

How Credit Score Affects Loan Interest Rate

How Lenders Use Credit Score for Risk-Based Pricing Banks and non-banking financial companies (NBFCs) do not always offer the same interest rate to every borrower. This is where risk-based pricing loan models come in. Th

Soft Inquiry vs Hard Inquiry

What Is a Soft Inquiry on Your Credit Report A soft inquiry (often called a soft pull) happens when your credit report is reviewed for reasons not tied to a formal application for a new loan or credit card. The most comm

CIBIL Score Showing -1 or NH?

What does CIBIL score -1 mean? The first thing to know is that a CIBIL score of -1 isn’t a sign of bad credit. In most situations, it simply means the credit bureau doesn’t have enough recent information to calculate a s

Rebuild CIBIL Score After Closing a Personal Loan

Does closing a personal loan affect CIBIL score? Yes, clearing your debt directly shapes your credit record, and it is entirely normal to see a sudden, temporary fluctuation. When you complete a repayment cycle, the lend

First-Time User's Guide to Building Your Credit Score

Why does your First Credit Score matter? Many people pay attention to their credit score only when they need a loan. By then, it can already be too late to improve it quickly. Your first credit score becomes the foundati

CIBIL Score for a Bike Loan

What is the Minimum CIBIL Score for a Bike Loan? One of the biggest misconceptions is that every lender requires a score of 750 or higher. That isn’t how bike loan approvals work. At present, there is no common or RBI-ma

Gold Loan and CIBIL Score

Is a CIBIL Score required for a Gold Loan? One myth associated with gold loans is that every individual requires a good credit score to apply for one. The CIBIL score for a gold loan is not important because it is secure

CIBIL Score for an Education Loan

What CIBIL Score is required for an Education Loan? Lenders evaluate the overall credit risk of a joint application using specific institutional scoring brackets. The definitive CIBIL score for education loan approval ty

How To Increase CIBIL Score from 500 to 750

Is it possible to increase CIBIL score from 500 to 750? Achieving a prime credit score of 750 from a baseline of 500 is entirely possible with a systematic approach. A score of 500 typically reflects past payment delays,

Reasons Your CIBIL Score Dropped Suddenly

Why Did My CIBIL Score Drop Suddenly? Your CIBIL score is not static it changes over time based on the latest information that banks and financial institutions report to the credit bureau, usually every month. As new rep

Does BNPL affect your credit score?

What is BNPL? Buy Now, Pay Later allows you to purchase without paying the full amount upfront. It is commonly offered at online checkouts and is also gaining acceptance among offline merchants. This facility makes short

Experian vs CIBIL Score

What is an Experian credit score? Experian is a prominent global credit information company operating in dozens of countries and entered the Indian market with authorization from the Securities and Exchange Board of Indi