Yes, if you operate a business/company or are a lender, you can download the Company Credit Report from the official portal of CIBIL. Also, you must have a valid membership with CIBIL to download the CCR.

- Home

- Credit Score

- Commercial Cibil Csgen

CIBIL Commercial Report : Check Complete Details on CCR

Get Your Credit Score & Report for Free, Forever!

- Instant Results

- No Hidden Fees

- Secure & Confidential

- No Impact on Your Credit Report

Get your Credit Score Report5 Lac+ people have got their Credit Scores for FREE!

+91

I agree to the Terms and Conditions of TUCIBIL and hereby provide explicit consent to share my Credit Information with Urban Money Private Limited.

Verify your number

Enter 6 Digit OTP

Change mobile number

Table of Content

Read more

A commercial CIBIL report is a type of document. It contains information about your business entity’s creditworthiness, such as CIBIL score, credit history, debt-to-income ratio, etc. When the entity’s owner applies for a business loan, the company CIBIL score is the first thing a lender may check. Whether the applicant owns a private limited company, public limited company, partnership firm, or proprietorship, the commercial CIBIL report provides the lender with a detailed insight into the company’s financial well-being and credit background. To learn more, continue to scroll down. Hereunder, Urban Money presents a comprehensive overview of commercial CIBIL. We primarily cover details such as how to get your CIBIL report, applicable features, factors affecting your company’s CIBIL score, how to improve your CIBIL score, etc.

How to Obtain Your CIBIL Commercial Report

For CIBIL commercial login, you need to follow the steps given below:

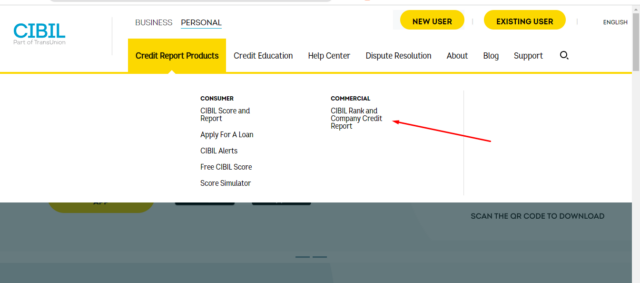

- Step 1: Visit the official website of CIBIL, a credit bureau company in India.

- Step 2: Go to the “Credit Report Product” menu and then select the “CIBIL Rank and Company Credit Report” option

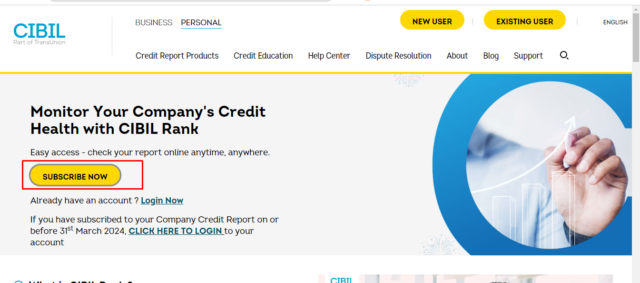

- Step 3: Tap on the “Subscribe Now” button.

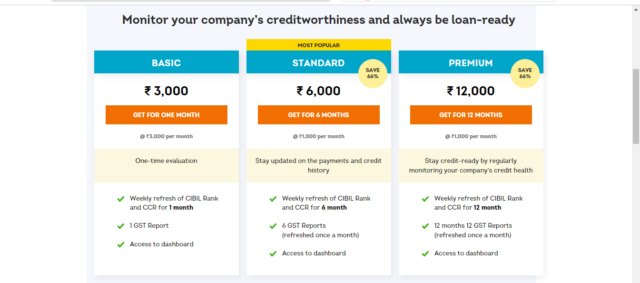

- Step 4: Choose the subscription plans that best suit you, enter the company details and complete the payment.

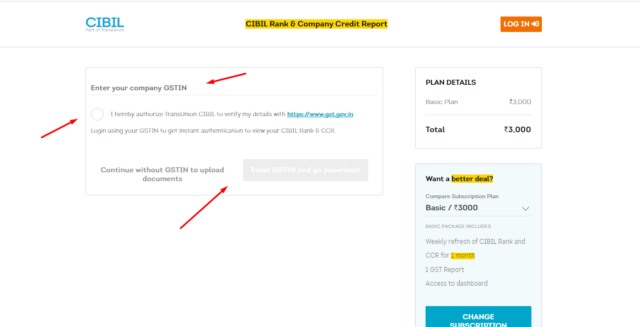

- Step 5: Complete the payment procedure and enter the company GSTIN Number

- Step 6: Upload the KYC documents and click the “Submit” button.

- Step 7: You will receive an email mentioning your transaction ID and registration ID

- Step 8: Your commercial CIBIL report will be mailed to your registered company address within a week.

Documents Required to Check CIBIL Commercial Report

Let’s examine the necessary documents you may require to check the company CIBIL score:

For Private and Public Limited Companies

If your company is registered as a private or public limited, then you have to present the following documents:

- Identity proof of one of the authorized signatories, which may include a Passport, PAN, or Driving License

- Anyone address proof from the following: passbook or bank account statement, telephone or electricity bill, sale agreement of office premises/registered lease, address proof issued by multinational or commercial banks, registration certificate issued under Shops & Establishment Act

- PAN card of the company

- A scanned copy of the board resolution along with the authorized specimen signature and signatory list

For Proprietorship

If you are a single owner of the business/company or have your business registered as a sole proprietorship; then you have to submit the following documents to check Commercial CIBIL Report:

- Proof of Identity of the proprietor, which could be a Driving License, PAN, or Passport

- Any of the following proof of address — registration certificate issued under the Shops & Establishment Act, electricity or telephone bill, etc

Note: The proprietor must self-attest all the above-mentioned documents.

For Partnership Firms

If you own a partnership firm with one or few other partners, then you must submit the following documents:

- PAN of the partnership firm

- Copy of certificate of registration or partnership deed

- Identity proof of partner requesting for the Company Credit Report, which may include Passport, Driving License, or PAN

- List of specimen signatures along with authorized signatories

Key Features of the CIBIL Commercial Report

Let’s examine the key features of the commercial CIBIL report:

- Company Background: It includes legal establishment, branches, ownership, and years of operation.

- Financial Information: It details the company’s credit standards based on financial data, such as outstanding loans, overdue, collateral, etc.

- CIBIL Rank: It reflects the company’s creditworthiness with a rank between 1 (highest) and 10.

- Credit History: It records the company’s financial history, including collections, repayments, and revenue generation.

Applicable Elements That Influence Your CIBIL Commercial Report

Here are the applicable elements that impact your company’s CIBIL score:

- Company Profile: The company profile mainly indicates the life and size of the corporation. Usually, older and bigger organisations have a well-established financial history. Therefore, they are considered more credible than startups and new businesses.

- Credit Repayment History: This refers to your repayment behaviour. Any default or late payment can significantly lower your credit score. On the other hand, paying your debt or EMI on time can enhance your overall commercial CIBIL report.

- Credit Utilisation Ratio: This is a metric represented by percentages. It signifies the difference between your total available credit limits and the amount you have utilised from that limit. Keeping your credit utilisation ratio low is considered ideal for a positive credit report, as the credit bureau company in India views this as a healthy financial habit.

- Credit Duration: This indicates the length of time you have been repaying your debt or EMI. Notably, the credit bureau in India views longer durations favourably, as they consider this a testament to responsible repayment. Thus, the longer the repayment period, the better the credit score.

- Outstanding Debts: This refers to any remaining debt you may have. Specifically, the total amount of money you must repay to be debt-free. Keeping your outstanding debt as low as possible helps improve your credit score, while higher outstanding debt can lower it.

- Credit Enquiries: This means how many credit applications you have raised. Multiple credit applications or inquiries in a short period can adversely affect your credit report. The credit bureau interprets this as credit-hungry behavior, indicating you may have experienced financial hardship.

- Industrial Sector: Specific industrial sectors have a higher risk and impact the company’s CIBIL Commercial Report. For instance, if your company operates in the oil and gas sector, deemed to have high volatility due to global market conditions, the lenders will consider your company less creditworthy compared to companies in other stable sectors like insurance and banking.

How to Improve Your CIBIL Commercial Report

Here are certain tips you can keep in mind to improve your commercial CIBIL report:

- Timely Payments: Ensure all dues are paid on time to maintain a good repayment history.

- Debt Management: Pay off debts to keep the outstanding debts feasible and your company’s repayment ability in good standing.

- Credit Utilisation: Lower your credit-to-debt ratio below 30% to maintain a balanced credit utilisation.

- Credit Enquiries: Avoid excessive hard inquiries in a short span of time, as this can indicate credit-hungry behaviour and cause a lower credit score.

- Financial Health: Maintain a long history of responsible credit behaviour and ensure your assets always exceed your liabilities.

Why Your CIBIL Commercial Report Matter

Let’s examine the importance of CIBIL commercial login:

- Loan Approval: A positive report can lead to quicker credit approvals and potentially better interest rates.

- Business Insights: It provides a comprehensive view of your business’s financial health and credit performance.

- Risk Mitigation: It helps lenders assess the level of risk associated with lending to your company.

Comparison of Commercial CIBIL vs Consumer CIBIL

Below is the comparison of commercial CIBIL and consumer CIBIL:

| Aspect | Commercial CIBIL | Consumer CIBIL |

| Target | Businesses and commercial entities | Individual consumers |

| Purpose | To assess the credit histories of business entities for loan eligibility | To assess the credit history of individuals for loan eligibility |

| Credit Model | CIBIL rank between 1 and 10 | CIBIL scores between 300 and 900 |

| Report Type | Commercial Credit Report | Credit Information Report (CIR) |

| Key Attributes | Payment history, credit mix, credit utilisation, financial stability | Number of accounts, loans, credit cards, repayment patterns |

Comparison of CIBIL Commercial Report vs Individual’s Credit Report

Below is the comparison of a company credit report and an individual Credit report:

| Aspect | CIBIL Commercial Report | Individual’s Credit Report |

| Focus | Creditworthiness and financial history of businesses | Creditworthiness of individuals |

| Aim | To evaluate credit risk and financial transactions with businesses | To evaluate credit risk with the individuals |

| Content | Business’s credit history, loan repayment, financial stability | Individual’s credit accounts, repayment history, outstanding debts |

| Scoring/Ranking | Rank between 1 (highest creditworthiness) and 10 | Score between 300 (lowest) to 900 (highest creditworthiness) |

| Analysis | A rank closer to 1 results in more favourable loan terms and interest rates | A higher score can lead to better loan terms and interest rates |

What Details Are Included in a CIBIL Business Credit Report

Following are the key details that are included in a commercial CIBIL report:

- Company Details: Company name, industry type, number of employees, legal constitution, etc.

- Contact Information: Registered office address, mobile number, telephone number, and fax numbers.

- Identification Details: Registration number, Taxpayer Identification Number (TIN), Corporate Identification Number (CIN), Service Tax Number, PAN card number, etc.

- Delinquency Reports: Financial creditworthiness of the company and guarantors, including current and past due status, outstanding amounts, etc.

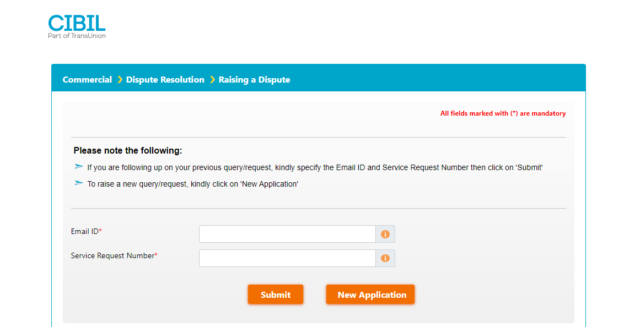

How do I Rectify Information on CCR?

If the information registered on your CCR seems incorrect, you can raise a dispute with CIBIL. The portal offers an online commercial dispute form where you can provide details of the dispute, such as —

- Company Name and Registered Address

- Branch Address, if any (optional)

- Name of Authorised Signatory

- Contact details such as your phone number and email address

- Company PAN

- Report Order Number — a unique 10-digit number that reflects on the top right-hand side of your Credit Information Report (CIR)

- Date of Report

- Reason for Dispute

Click on the following link to access the dispute form — https://www.cibil.com/online/file-company-dispute.do.

Once you have furnished the required information, enter the CAPTCHA code and click on the ‘Submit’ button.

| Related Guide |

| How is your CIBIL score calculated? |

| Written Off in CIBIL Reports |

| How to Check CIBIL Score with PAN Card |

Get your Credit Score Report worth ₹500 for FREE

5 Lac+ people have got their Credit Scores for FREE!

Last Updated: 24th July 2026

FAQs

Can lenders use a CIBIL commercial report to assess a business's creditworthiness?

Lenders can use a CIBIL commercial report to assess a business’s creditworthiness.

How frequently should businesses review their CIBIL commercial report?

Reviewing your CIBIL commercial report once a month is considered ideal.

Are there laws regulating CIBIL commercial reports?

The credit reporting agencies, including CIBIL, are directly regulated by the Reserve Bank of India (RBI).

Do strong CIBIL commercial reports help businesses get better financing?

Yes, having strong CIBIL commercial reports can help businesses obtain better finance and more favourable interest rates and terms.

What does Credit Order Number mean in CIBIL Commercial Report?

It’s a unique number generated every time somebody accesses your Company Credit Report from CIBIL’s database.

Who can access CIBIL rank and CCR?

CIBIL members, including financial institutions and banks, can access the CIBIL rank and CCR of any company applying for a loan.

Can I download the Company Credit Report?

Latest from the Credit Score Blog

Get in-depth knowledge about all things related to Credit Score and your finances

Aug 04, 2026

CIBIL Score for Mudra Loan

Is CIBIL score required for Mudra loan? Search for the Mudra loan CIBIL score online, and you’ll probably come away more confused than informed. One website claims you need a score of 650. Another pushes the figure to 70

Jul 23, 2026

CIBIL Score for Women Housewives and Homemakers

Why is a CIBIL score equally important for women? The credit score has become an essential factor for most lending decisions. It is used by banks and NBFCs to analyze a person’s previous experience in managing credit. Fo

Jul 23, 2026

Credit Score vs CIBIL Score

What is a credit score? A credit score is nothing but a three-digit number that shows how well you have been handling borrowed funds. It is generated from data such as loan repayments, credit card transactions, outstandi

Jul 23, 2026

How Credit Score Affects Loan Interest Rate

How Lenders Use Credit Score for Risk-Based Pricing Banks and non-banking financial companies (NBFCs) do not always offer the same interest rate to every borrower. This is where risk-based pricing loan models come in. Th

Jul 23, 2026

Soft Inquiry vs Hard Inquiry

What Is a Soft Inquiry on Your Credit Report A soft inquiry (often called a soft pull) happens when your credit report is reviewed for reasons not tied to a formal application for a new loan or credit card. The most comm

Jul 23, 2026

CIBIL Score Showing -1 or NH?

What does CIBIL score -1 mean? The first thing to know is that a CIBIL score of -1 isn’t a sign of bad credit. In most situations, it simply means the credit bureau doesn’t have enough recent information to calculate a s

Jul 23, 2026

Rebuild CIBIL Score After Closing a Personal Loan

Does closing a personal loan affect CIBIL score? Yes, clearing your debt directly shapes your credit record, and it is entirely normal to see a sudden, temporary fluctuation. When you complete a repayment cycle, the lend

Jul 13, 2026

First-Time User's Guide to Building Your Credit Score

Why does your First Credit Score matter? Many people pay attention to their credit score only when they need a loan. By then, it can already be too late to improve it quickly. Your first credit score becomes the foundati

Jul 13, 2026

CIBIL Score for a Bike Loan

What is the Minimum CIBIL Score for a Bike Loan? One of the biggest misconceptions is that every lender requires a score of 750 or higher. That isn’t how bike loan approvals work. At present, there is no common or RBI-ma

Jul 13, 2026

Gold Loan and CIBIL Score

Is a CIBIL Score required for a Gold Loan? One myth associated with gold loans is that every individual requires a good credit score to apply for one. The CIBIL score for a gold loan is not important because it is secure

Jul 13, 2026

CIBIL Score for an Education Loan

What CIBIL Score is required for an Education Loan? Lenders evaluate the overall credit risk of a joint application using specific institutional scoring brackets. The definitive CIBIL score for education loan approval ty

Jul 13, 2026

How To Increase CIBIL Score from 500 to 750

Is it possible to increase CIBIL score from 500 to 750? Achieving a prime credit score of 750 from a baseline of 500 is entirely possible with a systematic approach. A score of 500 typically reflects past payment delays,

Jul 10, 2026

Reasons Your CIBIL Score Dropped Suddenly

Why Did My CIBIL Score Drop Suddenly? Your CIBIL score is not static it changes over time based on the latest information that banks and financial institutions report to the credit bureau, usually every month. As new rep

Jul 10, 2026

Does BNPL affect your credit score?

What is BNPL? Buy Now, Pay Later allows you to purchase without paying the full amount upfront. It is commonly offered at online checkouts and is also gaining acceptance among offline merchants. This facility makes short

Jul 02, 2026

Experian vs CIBIL Score

What is an Experian credit score? Experian is a prominent global credit information company operating in dozens of countries and entered the Indian market with authorization from the Securities and Exchange Board of Indi