- Home

- Credit Score

- Check Axis Bank CIBIL Score

Axis Bank CIBIL Score: How to Check and Improve Your Axis CIBIL Score

Why is your credit score significant? A strong credit score, ideally between 750 and 900, is a game-changer. It can speed up your loan approval, reduce interest rates, and smoothen your loan applications. Axis Bank even specifies the minimum credit score required for a home loan, personal loan, and credit card. So, carefully monitor your credit score—it can significantly open your doors to financial assistance when you need it the most!

- Instant Results

- No Hidden Fees

- Secure & Confidential

- No Impact on Your Credit Report

I agree to the Terms and Conditions of TUCIBIL and hereby provide explicit consent to share my Credit Information with Urban Money Private Limited.

Verify your number

Enter 6 Digit OTP

Change mobile number

Table of Content

Last Updated: 12 July 2026

How To Check Axis Bank CIBIL Score

To check your Axis Bank CIBIL Score, make sure to follow these steps:

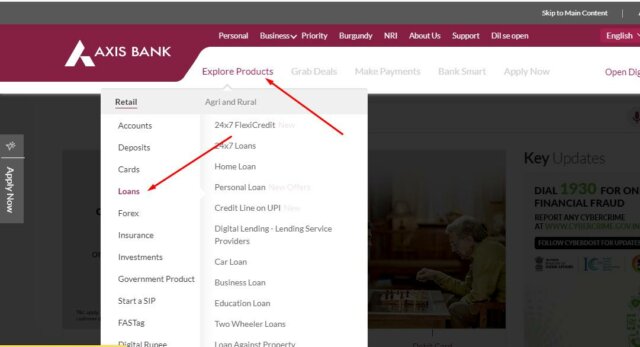

- Go to the official Axis Bank website.

- Navigate to “Explore Products” and select “Loans.”

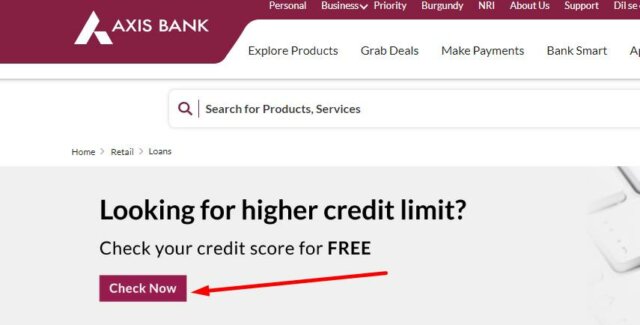

- Click on the Credit score banner.

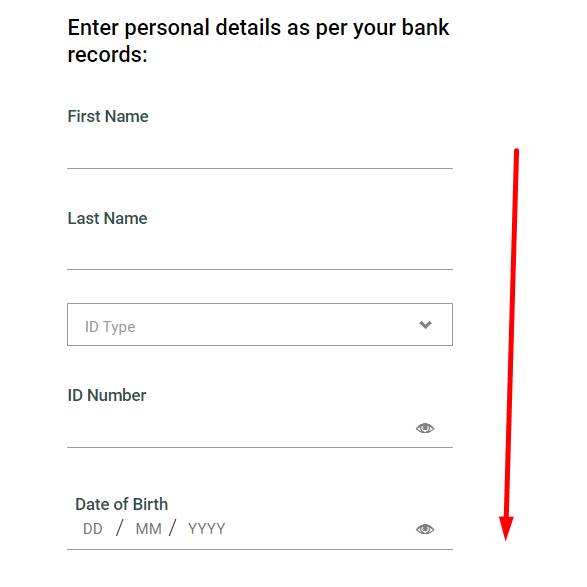

- Fill out the online form.

- Please enter your personal information, such as your email ID, name, date of birth, ID type, and mobile number.

- You will receive an OTP on your email address.

- Complete the registration process.

- Receive your complimentary credit report.

CIBIL Score for Axis Bank Home Loan

When you want to get a home loan from Axis Bank, your CIBIL score matters. Here’s the deal:

Your CIBIL score is like a report card of your borrowing history, with numbers from 300 to 900. The higher your score, the better you’ve handled credit in the past. But if it’s lower, there’s room to do better.

Axis Bank usually wants a home loan applicant with a score of at least 650. This number shows you are good at handling money and paying back what you owe. Moreover, your score also affects the interest you will pay on your loan. If your score is good, you will likely get a lower rate, saving you money in the long run. Other than that, a high CIBIL score might even get you a bigger loan than you requested. But if it’s low, you might not get as much as you hoped.

And here’s the kicker: if your score is high, you will probably get approved for your loan faster. But if it’s low, the bank might take longer to decide.

Axis CIBIL Score for Home Loan Eligibility

| Specification | Details |

| CIBIL Score | 750+ / 650-749 / <650 |

| Interest Rates | 8.50% – 9.50% |

| Processing Fees | 0.50% – 1% (Min: ₹10,000) |

| Prepayment | Floating: Nil / Fixed: Up to 2% |

| Loan Tenure | 5 to 30 years |

| Loan Amount | Min: ₹3 lakh / Max: ₹5 crore |

| Age | 21 to 65 years |

| Insurance | Required |

| Disbursement | 15-30 days |

| LTV | Max: 90% |

CIBIL Score for Axis Bank Personal Loan

Your CIBIL score is crucial to establish mutual trust between you and your lenders. It showcases how reliable you are with money by reflecting on your borrowing and repayment history. Lenders rely on your credit score to decide whether to give you that loan or establish strict rules to ensure timely repayments. Ideally, aim for a CIBIL score of 710 or higher. It increases your chances of loan approval and can give you better terms, like lower interest rates and more favorable conditions. But what if your score is lower, say around 600? Well, it’s a bit of a grey area. Some lenders might still consider scores under 710, but usually, they come with a catch—higher interest rates. It’s always good to check directly with the lender to see where you stand.

Now, what shapes your CIBIL score?

- First off, making timely payments is a huge plus. Paying your bills on time is like a gold star for your score.

- Also, keep your credit card spending in check. It’s better for your score if you don’t max out your cards.

- Lenders also consider how long you’ve been borrowing money. The longer your credit history, the better it looks on your record.

And here’s a tip: having a mix of different loans—like a home loan and a credit card—can boost your score. But watch out for credit inquiries. Every time you apply for a loan or a credit card, it leaves a mark on your record. Too many marks can temporarily bring your score down.

Axis CIBIL Score for Personal Loan Eligibility

| Specification | Details |

| CIBIL Score | 750+ / 700-749 / <700 |

| Interest Rates | 10% – 24% |

| Processing Fees | 1% of loan amount (Min: ₹10,000) |

| Prepayment | Floating: Nil / Fixed: Up to 2% |

| Loan Tenure | 1 to 5 years |

| Loan Amount | Min: ₹15,000 / Max: ₹25 lakh |

| Age | 21 to 60 years |

| Insurance | Optional |

| Disbursement | Within 3-5 days |

| LTV | N/A |

CIBIL Score Required for Axis Bank Credit Card

The applicant must have a decent credit score to be eligible for an Axis Bank credit card if the applicant’s borrowing and repayment history indicates that the applicant does not have a good repayment history.

The CIBIL Score required to qualify for an Axis Bank Credit Card is a minimum of 650 or higher. Holding a higher score allows the bank to develop mutual trust and increases your chances of securing a credit card with a generous spending limit. Occasionally, Axis Bank might consider issuing a credit card even if your score falls below this benchmark, particularly if you have a regular and healthy income and maintain a favourable debt-to-income ratio.

If your credit score is lower than expected, you still have a chance to avail of a credit card, but the eligibility criteria can become stringent. Thus, it is always advisable to hold a healthy credit score so that you can avail yourself of a credit card from any bank at any time.

What are the Factors Affecting Your Axis Bank CIBIL Score

Your CIBIL score is a crucial factor lenders look at when you’re applying for loans or credit cards. Let us take a look at the important factors that affect your cibil score:

- Payment History (35%): This is an important factor that affects your cibil score significantly. It shows if you are good at paying bills on time. Late payments or defaults can hurt your score, but being consistent helps.

- Credit Utilisation Ratio (30%): This is about how much of your credit you use compared to what you are given. Using too much can lower your score, so it’s smart to keep it low.

- Duration of Credit History (15%): The longer you have been using credit responsibly, the better it is for your score. New credit card users might have lower scores because they haven’t built enough history yet.

- Credit Mix and Variety: Having a mix of different types of credit, like loans and credit cards, can be good for your score. It shows you can handle different kinds of debt responsibly.

- Number of Credit Inquiries: Every time you apply for credit, it leaves a mark. Too many marks can bring your score down temporarily, so it’s best to keep applications to a minimum.

Range Table of Axis Bank CIBIL Score

Let us take a look at the table below to understand the different ranges of CIBIL scores and the category to which each range belongs:

| CIBIL Score | Interpretation |

| 300-549 | Poor Score: High risk to lenders |

| 550-699 | Average Score: Repayment hurdles but potential for improvements. |

| 700-749 | Good Score: A decent credit score reflecting responsible credit behaviour. |

| 750+ | Excellent: Qualifies for better loan deals |

Steps to Improve Your Low Axis Bank Credit Score

A below-average credit score indicates irresponsibility towards repayments, which results in the inability to establish trust between the applicant and the lender. If you have a below-average credit score and wish to improve it, here are the ways to improve your Axis Bank credit score:

- Timely Repayments: Pay your EMIs well before the due date. If you cannot pay on time, an interest rate will apply to the defaulted payments, lowering your credit score. Hence, timely repayments are crucial to maintaining or improving your credit score.

- Settle Your Past Dues: If you have any credit outstanding, make sure you pay that on time. Spending more than your budget and unable to pay your EMIs will result in consolidated debt, lowering your credit score significantly.

- Wise Usage of Credit Cards: Spending too much than required, knowing it exceeds your budget and might result in defaulted repayments, is not wise. Hence, take note of your budget and realise the maximum EMI you can afford to pay. Also, timely repayments are crucial. Therefore, moderate usage with timely repayments is one of the best ways to improve your credit score.

Latest from the Credit Score Blog

Get in-depth knowledge about all things related to Credit Score and your finances

First-Time User's Guide to Building Your Credit Score

Why does your First Credit Score matter? Many people pay attention to their credit score only when they need a loan. By then, it can already be too late to improve it quickly. Your first credit score becomes the foundati

CIBIL Score for a Bike Loan

What is the Minimum CIBIL Score for a Bike Loan? One of the biggest misconceptions is that every lender requires a score of 750 or higher. That isn’t how bike loan approvals work. At present, there is no common or RBI-ma

Gold Loan and CIBIL Score

Is a CIBIL Score required for a Gold Loan? One myth associated with gold loans is that every individual requires a good credit score to apply for one. The CIBIL score for a gold loan is not important because it is secure

CIBIL Score for an Education Loan

What CIBIL Score is required for an Education Loan? Lenders evaluate the overall credit risk of a joint application using specific institutional scoring brackets. The definitive CIBIL score for education loan approval ty

How To Increase CIBIL Score from 500 to 750

Is it possible to increase CIBIL score from 500 to 750? Achieving a prime credit score of 750 from a baseline of 500 is entirely possible with a systematic approach. A score of 500 typically reflects past payment delays,

Reasons Your CIBIL Score Dropped Suddenly

Why Did My CIBIL Score Drop Suddenly? Your CIBIL score is not static it changes over time based on the latest information that banks and financial institutions report to the credit bureau, usually every month. As new rep

Does BNPL affect your credit score?

What is BNPL? Buy Now, Pay Later allows you to purchase without paying the full amount upfront. It is commonly offered at online checkouts and is also gaining acceptance among offline merchants. This facility makes short

Experian vs CIBIL Score

What is an Experian credit score? Experian is a prominent global credit information company operating in dozens of countries and entered the Indian market with authorization from the Securities and Exchange Board of Indi

How Credit Utilisation Ratio Affects CIBIL Score

What is credit utilization ratio? The basic credit utilization ratio meaning centers on a simple comparison: it is the ratio of your total outstanding credit card balances to your total credit card limits. If you hold mu

Credit Score Monitoring

Why is credit monitoring important? Credit monitoring goes a long way in protecting and improving your financial health. Regularly reviewing your credit information can help you identify reporting errors or outdated deta

What is a Credit Report?

Why do credit reports matter? Two people can apply for the same loan with similar incomes and still receive different outcomes. One reason is the information sitting inside their credit reports. Lenders don’t just want t

CRIF Credit Score Free Check

What is the CRIF High Mark credit score? The CRIF High Mark credit score is a three-digit number that assesses your creditworthiness by tracking your past debt history. CRIF High Mark is one of the four core credit burea

Check Poonawalla CIBIL Score for Free

How to check CIBIL score on Poonawalla? A Poonawalla CIBIL check can be completed online within a few minutes. The platform allows users to access their TransUnion CIBIL score after basic identity verification. To begin,

Check Piramal CIBIL Score for Free

How to check the free CIBIL score on Piramal? You can access your complete credit assessment through the digital portal of Piramal Finance without incurring any processing charges. Piramal has simplified this process by

Factors Affecting Your Credit Score

What factors affect your credit score? Credit bureaus calculate credit scores using multiple aspects of your borrowing and repayment behavior. There is no single factor that determines your score; instead, several elemen