- Home

- Credit Score

- Cibil Report Access Download

How to Check, Download, and Understand Your CIBIL Report

- Instant Results

- No Hidden Fees

- Secure & Confidential

- No Impact on Your Credit Report

I agree to the Terms and Conditions of TUCIBIL and hereby provide explicit consent to share my Credit Information with Urban Money Private Limited.

Verify your number

Enter 6 Digit OTP

Change mobile number

Table of Content

Last Updated: 11 July 2026

Do you often find that your credit score is limiting your opportunities? If yes, then you are not alone! But what if you could unlock better loan rates, lower insurance premiums, and even your dream rentals by improving your CIBIL score? The path to financial freedom starts with realising the power of your CIBIL score.

A credit score is a numerical representation of an individual’s creditworthiness, used to assess their ability to repay borrowed funds. Typically ranging from 300 to 900, the highest score signifies a reliable borrower. Having a high credit score for loan and credit card applications is good. If your score is low or in the lower range, you haven’t been responsible for paying back loans or debts on time.

A strong CIBIL score can be your greatest asset, from effortlessly securing loans to negotiating improved credit terms. However, this number remains a hurdle for many because of misunderstandings and miscommunication.

We will help you improve your financial standing. This will involve making payments on time and using credit wisely. Through this blog, we aim to ensure your CIBIL score accurately represents your ability to borrow money.

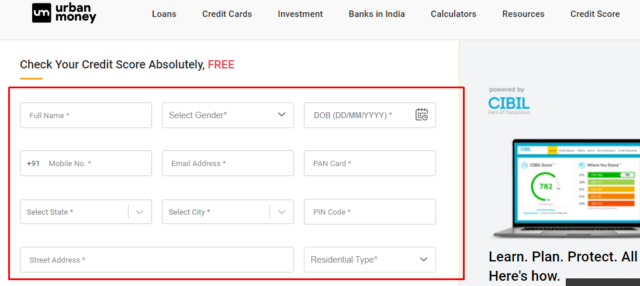

How do you check and download the CIBIL Report?

Here are three simple steps to access your CIBIL score via Urban Money without charges.

- Step 1: Go to our credit score webpage. (https://www.urbanmoney.com/credit-score)

- Step 2: Fill in your personal information, such as your Name, Mobile Number, and Email Address. Experian will send you a one-time password (OTP) to your provided phone number.

- Step 3: Verify the OTP, and your credit report will appear on the screen. Experian will also send a copy to your registered email address. You can download the report as a PDF file if you prefer.

Components of a CIBIL Report

A CIBIL report, also known as a credit information report (CIR), is a detailed document that provides an overview of an individual’s credit history and score. Compiled by the Credit Information Bureau (India) Limited (CIBIL), this report plays an important role in a lender’s decision-making process regarding loan approvals and interest rates offered to the borrower.

Here are the key components of a CIBIL report:

- CIBIL Score: The CIBIL credit bureau determines a CIBIL score between 300 and 900 based on factors like credit history and repayment patterns. A score between 750 and 900 is considered favorable. A higher CIBIL score indicates that you are highly creditworthy, which improves your likelihood of obtaining favourable loan interest rates and credit card offers.

- Personal Information: This section contains all your personal details, such as your name, date of birth, and unique identification numbers, such as PAN and Aadhaar. It is important to double-check that the information provided is correct. The bank is responsible for submitting these details to the bureau.

- Contact Information: This section will include your phone number, landline number, home address, and email address.

- Employment Information: This section of the CIBIL report details your job. It will indicate the nature of your work, such as whether you are a salaried employee, a professional, or a businessperson. Additionally, it will state the amount of money you earn monthly or yearly, as reported by banks.

- Account Information: The CIBIL report provides important information about your credit accounts, including loans, cards, defaults, late payments, outstanding amounts, current balances, account opening dates, and most recent payments.

- Enquiry Information: This section records past lender enquiries, including dates, purposes, and amounts. It advises against making multiple inquiries frequently to avoid appearing credit-hungry and triggering hard inquiries from lenders.

- Days Past Due (DPD): Indicates the number of days a payment on an account is late. A value of “000” means payments were made on time, while any other number indicates a delay in payment for that many days.

Importance of a CIBIL Report

Lenders like to review your credit report when you request a loan or credit card, as it reveals your creditworthiness. By examining your past borrowing behaviour, they can determine if you have been a responsible borrower. A CIBIL report showcasing timely payments, minimal credit inquiries, and a positive credit history will increase your likelihood of getting loan approval.

Factors Affecting the CIBIL Score

The following are some significant factors that affect your credit score:

Loan Repayment History: Paying your loans on time can significantly improve your credit score. However, failing to make your EMIs or late payments will negatively affect your CIBIL score. Your repayment history plays an important role in determining your CIBIL score.

Credit History Duration: The length of time you have been using credit cards or loans and consistently making payments on them also plays a role in determining your credit score. A history of responsible credit behaviour over a significant period demonstrates discipline. This factor has a moderate impact on your overall credit score.

Number of Inquiries: When you apply for a new credit item, the lender looks into your credit score. We call these inquiries by lenders and financial institutions “hard inquiries.” A substantial number of hard inquiries indicates a strong need for credit, which will lower your credit score. In the near term, having several hard inquiries at once might greatly influence your credit score. On the other hand, obtaining or reviewing your credit report is regarded as a Soft Inquiry and does not affect your credit score.

Credit Utilisation Ratio (CUR): It refers to the proportion of your credit spending to the amount you can access. Maintaining a CUR below 30% of your available credit limit is advised. Even if your CUR is slightly higher, it will not significantly affect your credit score as long as you make timely payments on your credit card bill. However, consistently reaching the maximum limit on your credit card may indicate a strong reliance on credit, which can influence your credit score.

Mix of Credit: If you have responsibly repaid your different loans, such as personal, auto, or home loans, it demonstrates your ability to manage different types of credit. This gradual development of a favourable credit mix can positively influence your credit profile. On the contrary, if you have taken on an excessive amount of unsecured loans, it suggests a strong desire for credit and an excessive reliance on it. While this may impact your credit score, it is unlikely to be significant if your repayment history is strong. However, it is important to note that having several active loans simultaneously can result in a high “EMI to NMI ratio,” which may reduce your chances of getting additional credit.

In addition to the five main factors mentioned above that determine your CIBIL score, other elements can also affect it. These include mistakes in your credit report, a limited credit history, and an inability to fulfil your responsibilities as a loan guarantor. While these factors may negatively impact your credit score, they are not as significant as the primary factors.

Importance of Reviewing CIBIL Credit Report Regularly:

Monitoring your credit report is important to stay informed about your credit score. This report contains important details such as personal information, account specifics, payment history, outstanding balance, Days Past Due (DPD), if applicable, as well as active and closed accounts, recent inquiries, and collateral/security information. Most lenders require this information to process new credit applications.

By regularly checking your credit report, you can identify any errors or inaccurate/incomplete information that may impact your creditworthiness and potentially lower your credit score. If you discover any errors, it is important to report and resolve them promptly by submitting an online dispute resolution form through CIBIL’s official website using the Consumer Dispute Resolution Process.

Impact of CIBIL Credit Report on Loan Approvals

The CIBIL credit report is important in India’s loan approval process. Its impact on loan approvals is significant for several reasons:

Assessment of Creditworthiness: Lenders use the CIBIL report as a primary tool to assess an applicant’s creditworthiness. It helps them evaluate the risk associated with lending to the individual.

Interest Rates: Applicants with higher CIBIL scores often qualify for loans with more favourable interest rates. Lenders view them as low-risk borrowers willing to offer loans at lower rates.

Loan Amount and Tenure: The CIBIL report also impacts the loan amount and tenure that lenders are willing to offer. A strong credit history can lead to higher loan amounts and more flexible repayment periods.

Quick Processing and Approval: A clean and strong CIBIL report can lead to quicker loan processing.

Pre-approved Offers: Individuals with excellent credit histories often receive pre-approved loan offers based on the lender’s assessment of the CIBIL report. These offers come with expedited approval processes and attractive terms.

Impact on Unsecured Loans: Unsecured loans, such as personal loans and credit cards, rely heavily on the CIBIL report for approval, given the lack of collateral. A good report is essential for approval and favourable terms.

Risk Evaluation: The repayment history and credit utilisation ratio detailed in the report give lenders insight into the applicant’s financial management skills, which are necessary for unsecured loan approvals.

Better Negotiating Power: Applicants with high CIBIL scores have better leverage in negotiating loan terms, including interest rates, processing fees, and repayment schedules.

Documents Required for the CIBIL Credit Report

To get your CIBIL credit report, you must submit a request to CIBIL online or by mail. The process involves verifying your identity to ensure that sensitive financial information is securely and correctly handed over. Here is a list of documents commonly required to get your CIBIL report:

- Identity Proof: PAN Card/ Aadhaar Card/ Passport/ Voter ID Card/ Driver’s License

- Address Proof: Aadhaar Card/ Passport/ Voter ID Card/ Utility bills (electricity, water, gas) not older than 3 months/ Bank statements or passbook with current address/ Rental agreement or lease deed

CIBIL Customer Care

Contact CIBIL customer care via

Phone: Monday to Friday (10:00 a.m. to 6:00 p.m.)

+91-22-6140-4300

Fax:

+91 – 22 – 6638 4666

Address:-

TransUnion CIBIL Limited (Formerly: Credit Information Bureau (India) Limited)

One Indiabulls Centre, Tower 2A, 19th Floor, Senapati Bapat Marg, Elphinstone Road, Mumbai – 400013

Website:

To get in touch, simply go to https://www.CIBIL.com and click on ‘Contact Us’. Select ‘To Contact Us Online’ from there and click ‘Click here’. Fill in the required information and hit ‘Submit’.

FAQs

Can I access my CIBIL credit report for free?

You can access your CIBIL credit report for free simply by visiting https://www.urbanmoney.com/credit-score.

How do you download the CIBIL report PDF for free?

You get scores from multiple bureaus when you check your credit score on Urban Money. Your CIBIL report is provided on the dashboard where your CIBIL score is published. You can download the PDF of your CIBIL report here and use DDMMYYYY as the password.

How is the CIBIL score calculated?

Your CIBIL score is calculated based on various factors evaluated by credit bureaus or Credit Information Companies (CICs). These factors reflect your previous credit actions and are shared with Banks and NBFCs whenever you seek new credit.

How can I pay for the credit report?

Payment for the credit report can be made using various methods such as a demand draft, credit card, debit card, or through net banking.

What if I send the wrong details by mistake?

If you send the wrong details while requesting your credit report, you should immediately contact the credit bureau’s customer service to correct the information.

Latest from the Credit Score Blog

Get in-depth knowledge about all things related to Credit Score and your finances

CIBIL Score for an Education Loan

What CIBIL Score is required for an Education Loan? Lenders evaluate the overall credit risk of a joint application using specific institutional scoring brackets. The definitive CIBIL score for education loan approval ty

How To Increase CIBIL Score from 500 to 750

Is it possible to increase CIBIL score from 500 to 750? Achieving a prime credit score of 750 from a baseline of 500 is entirely possible with a systematic approach. A score of 500 typically reflects past payment delays,

Reasons Your CIBIL Score Dropped Suddenly

Why Did My CIBIL Score Drop Suddenly? Your CIBIL score is not static it changes over time based on the latest information that banks and financial institutions report to the credit bureau, usually every month. As new rep

Does BNPL affect your credit score?

What is BNPL? Buy Now, Pay Later allows you to purchase without paying the full amount upfront. It is commonly offered at online checkouts and is also gaining acceptance among offline merchants. This facility makes short

Experian vs CIBIL Score

What is an Experian credit score? Experian is a prominent global credit information company operating in dozens of countries and entered the Indian market with authorization from the Securities and Exchange Board of Indi

How Credit Utilisation Ratio Affects CIBIL Score

What is credit utilization ratio? The basic credit utilization ratio meaning centers on a simple comparison: it is the ratio of your total outstanding credit card balances to your total credit card limits. If you hold mu

Credit Score Monitoring

Why is credit monitoring important? Credit monitoring goes a long way in protecting and improving your financial health. Regularly reviewing your credit information can help you identify reporting errors or outdated deta

What is a Credit Report?

Why do credit reports matter? Two people can apply for the same loan with similar incomes and still receive different outcomes. One reason is the information sitting inside their credit reports. Lenders don’t just want t

CRIF Credit Score Free Check

What is the CRIF High Mark credit score? The CRIF High Mark credit score is a three-digit number that assesses your creditworthiness by tracking your past debt history. CRIF High Mark is one of the four core credit burea

Check Poonawalla CIBIL Score for Free

How to check CIBIL score on Poonawalla? A Poonawalla CIBIL check can be completed online within a few minutes. The platform allows users to access their TransUnion CIBIL score after basic identity verification. To begin,

Check Piramal CIBIL Score for Free

How to check the free CIBIL score on Piramal? You can access your complete credit assessment through the digital portal of Piramal Finance without incurring any processing charges. Piramal has simplified this process by

Factors Affecting Your Credit Score

What factors affect your credit score? Credit bureaus calculate credit scores using multiple aspects of your borrowing and repayment behavior. There is no single factor that determines your score; instead, several elemen

TransUnion CIBIL Score & Report

What is the TransUnion CIBIL score? A TransUnion CIBIL score is a three-digit number that represents an individual’s credit health based on their borrowing and repayment history. It is calculated using information such a

What is a Credit Information Report?

What is a Credit Information Report (CIR)? A credit information report a detailed document that records an individual’s credit history and borrowing behavior. It is essentially a summary of your loans, credit cards, repa

Check Equifax Credit Score

What is an Equifax Credit Score? An Equifax Credit Score is a number between 300 and 900 that reflects your credit history and repayment habits. It is calculated using information from your credit accounts, including loa