Best Travel Credit Cards 2026

Travel rewards

Cover included

- Home

- Credit Card

- Best Travel Credit Cards

Popular Travel Credit Card Offers

Scout through some of the best hand-picked credit card offers.

Categories

Cashback

Online Shopping

Lifetime Free

Rewards

Shopping

Fuel

Movies

Travel

Dining

Premium

Lounge Access

Filter

Banks

BOB Credit Card

Yes Pop-Club Credit Card

IndusInd Bank

HSBC Credit Card

IDFC First Credit Card

SBI Credit Card

Axis Credit Card

AU Small Finance Credit Card

HDFC Credit Card

BOBCARD Eterna

Travel

Movies

Shopping

Joining Fee: Nil

Annual/Renewal Fee: Nil

- Points can be redeemed for cashback or products.

- Zero liability on lost cards, contactless payments, and fraud protection.

- Smart EMI options to convert purchases above ₹2,500 into EMIs.

+ More Details

YES Private

Travel

Rewards

Premium

Joining Fee: ₹50,000 + taxes

Annual/Renewal Fee: ₹10,000 + taxes

- 2X rewards on international spends.

- Unlimited domestic & international visits.

- Exclusive privileges with premium hotels.

+ More Details

BOBCARD Premier

Travel

Dining

Shopping

Joining Fee: ₹1,000

Annual/Renewal Fee: ₹1,000

- Earn rewards for every spent upto ₹100.

- Get next year’s annual fee waived on ₹1,20,000 annual spend.

- Enjoy 4 complimentary airport lounge visits per year.

+ More Details

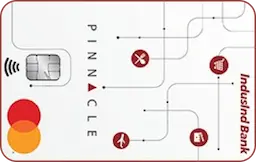

Pinnacle World Credit Card

Travel

Rewards

Online Shopping

Joining Fee: ₹15,000 + Taxes

Annual/Renewal Fee: ₹0

- Offer on movie tickets book with BookMyShow.

- Upto 1 international/domestic lounge visit.

- Membership for VIP access to airport lounges for up to 8 visits every year.

+ More Details

HSBC TravelOne Credit Card

Rewards

Travel

Joining Fee: ₹999 + taxes

Annual/Renewal Fee: ₹999 + taxes

- Complimantary visits to domestic/international lounges.

- 12 Complimantary golf lessons per year.

- 0 annual fee on ₹8L+ spend in a year.

+ More Details

FIRST Wealth Credit Card

Travel

Lifetime Free

Rewards

Joining Fee: Nil

Annual/Renewal Fee: Nil

- Upto 10X rewards on monthly spends.

- Up to 4 airport lounge visits per quarter

- Upto 5% cashback on your 1st EMI transaction.

+ More Details

Legend Credit Card

Travel

Lifetime Free

Rewards

Joining Fee: ₹0

Annual/Renewal Fee: ₹0

- Personal air accident insurance cover.

- Priority Pass with 600+ Airport Lounges access.

- Activation benefits from Luxe gift card, Montblanc, Post Card and vouchagram.

+ More Details

SBI Card PRIME

Travel

Shopping

Rewards

Joining Fee: ₹2,999 + Taxes

Annual/Renewal Fee: ₹2,999 + Taxes

- Vouchers on shopping from Bata, Hush Puppies, Pantaloons, Shoppers Stop, Aditya Birla, Yatra.

- Complimentary domestic/international lounge visits yearly.

- 5X rewards on dining, movies & grocery.

+ More Details

AXIS BANK ATLAS Credit Card

Travel

Lounge Access

Rewards

Joining Fee: ₹5,000 + taxes

Annual/Renewal Fee: ₹5,000 + taxes

- Complimentary international & domestic lounge access.

- 2,500 bonus EDGE Miles on card activation.

- Extra Platinum Tier Benefits.

+ More Details

AU Zenith+ Credit Card

Travel

Movies

Rewards

Joining Fee: ₹4,999 + Taxes

Annual/Renewal Fee: ₹4,999 + Taxes

- Up to 16 complimentary movies tickets.

- Upto 16 domestic/international lounge access.

- Buy 1 Get 1 Free movie ticket on BookMyShow.

+ More Details

BOBCARD Tiara

Movies

Shopping

Travel

Joining Fee: ₹2,499

Annual/Renewal Fee: ₹2,499

- Women's special card with more benefits.

- Get next year’s annual fee waived on ₹2,50,000 annual spend.

- Enjoy a complimentary 12-month FitPass Pro membership worth ₹48,000.

+ More Details

REGALIA GOLD Credit Card

Travel

Shopping

Rewards

Joining Fee: ₹2,500 + taxes

Annual/Renewal Fee: ₹2,500 + taxes

- Upto 5X rewards on Nykaa, Myntra & more.

- Complimentary domestic & international lounge access.

- Gift voucher worth Rs. 2,500 on payment of joining fee.

+ More Details

MARQUEE Credit Card

Travel

Rewards

Premium

Joining Fee: ₹9,999 + taxes

Annual/Renewal Fee: ₹4,999 + taxes

- Up to 4.5% back as reward points.

- Save up to Rs. 2,400 per month on BookMyShow.

- 1% fuel surcharge waiver up to ₹1,000/month on spends.

+ More Details

AU Zenith Credit Card

Travel

Dining

Rewards

Joining Fee: ₹7,999+ Taxes

Annual/Renewal Fee: ₹7,999 + Taxes

- Vouchers worth Rs. 1,000 on spends of Rs.2 Lac.

- Upto 2 domestic/international lounge access.

- Upto 2 lounge access at railway stations.

+ More Details

AXIS BANK RESERVE Credit Card

Travel

Rewards

Premium

Joining Fee: ₹50,000 + taxes

Annual/Renewal Fee: ₹50,000 + taxes

- Low foreign currency markup fee of 1.5%.

- 15 Edge Reward Points for every Rs. 200 spent.

- Complimentary lounge access domestic/international.

+ More Details

MARRIOTT BONVOY Credit Card

Travel

Lounge Access

Joining Fee: ₹3,000

Annual/Renewal Fee: ₹3,000

- Up to 8 Marriott Bonvoy Points on your spends.

- Up to 24 free lounge visits in a year.

- Upto 2 complimentary golf access per quarter across the globe.

+ More Details

INFINIA METAL Credit Card

Travel

Premium

Rewards

Joining Fee: ₹12,500 + taxes

Annual/Renewal Fee: ₹12,500 + taxes

- Unlimited domestic & international lounge access.

- Save on your stay at ITC and Marriott Hotels.

- Hotel and Dining Benefits with ITC Hotels

+ More Details

DINERS BLACK METAL Credit Card

Travel

Premium

Rewards

Joining Fee: ₹10,000

Annual/Renewal Fee: ₹10,000

- Exclusive discounts at spas, gyms, hotels & wellness.

- 24×7 concierge for dining, golf & car rentals.

- Free premium memberships on Rs. 1.5L spend in 90 days.

+ More Details

AXIS BANK MAGNUS Credit Card

Travel

Premium

Rewards

Joining Fee: ₹30,000 + taxes

Annual/Renewal Fee: ₹30,000 + taxes

- Complimentary domestic/international lounge access.

- 5X rewards on travel spends.

- Other Travel Benefits

+ More Details

What are Travel Credit Cards?

Travel credit cards are built for people who often spend on flights, hotels, cabs, and holiday bookings. Instead of offering only standard points, these cards focus on travel points, air miles, or flexible reward currencies that can later be redeemed for flights, upgrades, or hotel stays. Cards such as the HSBC TravelOne Credit Card show how these rewards grow faster when you book travel directly or through partner platforms.

Most travel cards also offer comfort perks such as lounge access, reduced foreign exchange markup, and early check-in benefits through airline and hotel partners. A few premium variants go even further, offering concierge services and additional travel protections. The purpose stays simple: combine everyday spending with meaningful travel returns.

Key Features of Travel Credit Cards

- Travel credit cards are built around how you actually travel, not just how much you swipe. They reward bookings, airport time, and even your spending abroad in ways a standard card typically does not. A card like the HDFC Regalia Gold Credit Card is a good example of how these features come together for someone who flies a few times a year and spends regularly on trips.

- Higher rewards on travel spends: When you book flights, hotels, or holiday packages, you usually earn more credit card rewards points or travel points than on routine spends. This is what makes the best travel cards stand out. A larger share of your travel budget gradually returns as points you can redeem later.

- Airport lounge access: Most solid travel credit cards include complimentary lounge visits. Instead of sitting at a crowded gate, you get a quieter space with basic food and seating. For frequent flyers, this becomes one of the most valuable credit cards for travel perks.

- Rewards that convert into flights and stays: The points you earn do not sit idle. They can be redeemed for flights, hotel stays, upgrades, or vouchers. Some of the best credit cards for travel points let you use a bank portal to book tickets directly, while others allow transfers to airline or hotel partners.

- Better support for international travel: Many good travel cards offer a lower foreign exchange markup than standard cards. That means card payments abroad for food, shopping, or transport incur lower fees. For someone who travels overseas even once a year, this matters more than it seems at first.

- Extra protections and add-ons: Selected top travel cards include travel insurance, lost baggage coverage, and accidental air travel protection. These are not always headline benefits, but they help when something goes wrong on a trip.

- Milestone bonuses and fee relief: If you use your card for most of your yearly travel and big spends, you often unlock milestone bonuses or annual fee waivers. That is where the best credit card for rewards and travel quietly pays for itself over time.

Types of Travel Credit Cards

Travel credit cards fall into a few clear categories, each built around a different way to earn and redeem travel points. Some work best for flight-heavy travellers, while others suit people who mix holidays with everyday spending. A card like the ICICI Bank Sapphiro Credit Card demonstrates how one product can fit multiple travel patterns, depending on how you use it.

- General travel rewards cards : These cards earn flexible credit card rewards points on most purchases and offer a higher rate when you book flights or hotels.

- Co-branded airline or travel programme cards : Some cards are linked directly to a travel brand. They earn travel-specific points or air miles that are redeemable in a single loyalty programme.

- Premium lifestyle travel cards : Premium travel cards focus on comfort as much as rewards. They include airport lounge access, concierge services, lower foreign exchange fees, and higher milestone and annual bonus payouts.

How do Travel Credit Cards Differ from Regular Credit Cards?

A travel credit card differs from an everyday rewards card because it focuses on what travellers spend most. With a card like the ICICI Bank Emeralde Credit Card, you can see how the structure shifts from general purchases to travel-specific value.

Regular cards reward purchases at the same flat rate for shopping, dining, or utility payments. Travel cards, on the other hand, usually give a higher return when you book flights, hotels, or use online travel platforms. The points you earn can be redeemed for flights, hotel stays, upgrades, or partner vouchers, not just merchandise.

Another clear difference comes from the perks. Many top-rated travel credit cards offer complimentary airport lounge access, travel insurance, and a lower foreign exchange markup, all of which benefit frequent and occasional flyers. Regular cards rarely offer these without limitations.

How do Travel Credit Cards Work?

When you make your usual payments like flights, hotel bookings, or even routine purchases, the card starts collecting travel points or miles based on how much and where you spend. A card like the YES Private Credit Card shows how this works in practice, especially when a bank offers higher returns on travel-related spends.

When you use a travel card for bookings, you generally earn a faster rate of points. These points sit in your account until you choose how to use them. Some cards let you redeem them directly for flights or hotel stays through the bank’s travel portal. Others allow transfers to airline or hotel partners, giving you greater flexibility to choose routes, dates, or room upgrades.

The perks run alongside the reward system. Airport lounge visits follow simple rules: either a fixed number of complimentary entries per quarter or entries unlocked after a minimum monthly spend. Purchases made abroad are billed at a lower foreign exchange markup than those on regular cards, making international trips more budget-friendly.

Everything comes together in your monthly statement, where you can track points earned, points redeemed, and how close you are to unlocking any best travel bonus credit cards milestone for the year.

Eligibility Criteria For Travel Credit Cards

Travel credit cards typically have higher eligibility requirements than basic rewards cards because they offer lounge access, travel perks, and stronger reward structures. A product like the Pinnacle World Credit Card provides a clear sense of the profile banks look for when approving premium, travel-focused cards.

- Age: Usually 21 to 60 years for salaried applicants and up to 65 years for self-employed users.

- Income: Minimum monthly income starts at approximately ₹30,000 for entry-level travel cards and can exceed ₹1,00,000 for premium cards.

- Credit score: A score above 700 improves approval chances; lower scores may still qualify for basic variants with smaller limits.

- Employment stability: Regular employment or steady business income over six months is often required.

- Nationality and residency: Indian citizens or residents with valid proof of address may apply; foreign nationals generally require local address documentation.

- Existing card record: Banks review current credit usage and repayment discipline before issuing a new card.

These criteria help ensure users can manage the features and spending requirements of the best travel credit card products comfortably.

Documents Required for Travel Credit Cards

When you apply for a travel credit card, the bank typically requests a few standard documents to verify your identity, address, and income. This verification process is consistent across premium cards, including the FIRST Wealth Credit Card, which undergoes rigorous KYC checks before approval.

- Identity proof: A PAN card is compulsory. You can pair it with Aadhaar, a passport, a voter ID, or a driving licence for identity verification.

- Valid address proof includes Aadhaar, a passport, a recent utility bill, or a registered rental agreement. The address you submit should match the one you provide in the application.

- Income proof: Salaried applicants can submit recent salary slips or Form 16. Self-employed applicants typically provide the latest ITRs or audited financial statements, depending on the bank’s requirement.

- Photograph: Some banks request a recent passport-sized photograph during physical or in-person verification.

- KYC verification: Banks now complete KYC digitally or through a short in-person check. Online applications usually move faster if your PAN and Aadhaar are linked.

How to Apply for Travel Credit Cards through Urban Money?

Applying for a travel credit card on Urban Money stays simple. The platform lets you compare travel rewards, lounge access, and international benefits side by side.

- Visit the Urban Money website and open the credit card tab from the main menu. In the dropdown, choose credit cards, then apply the travel filter to view options that match your trip style.

- Select the card you want and click Apply Now.

- Enter your name, mobile number, email, and PAN in the form, then submit it.

- Urban Money contacts you after submission to share the best available travel offers and bank instructions.

Why Use a Travel Credit Card?

A travel credit card adds value every time you book a flight, reserve a hotel room, or make everyday purchases that later convert into travel points. It helps frequent travellers save money, but it also benefits anyone who takes a few trips a year. A card like the AU Zenith Credit Card shows how travel-focused perks can make your journeys smoother without changing the way you spend.

One of the most significant advantages is the accelerated reimbursement of travel expenses. When you book tickets or stays through airline sites, hotel platforms, or online travel agencies, you earn more points than you would with a regular card. Those points can later be redeemed for flights, upgrades, hotel rooms, or partner vouchers.

Fees for Travel Credit Cards

Every travel credit card has its own cost structure. Most charge a joining fee at issuance and an annual renewal fee afterwards, both tied to the card’s reward tier.

| Travel Credit Card | Joining Fee | Annual / Renewal Fee | Condition | Indicative Forex

Markup |

| ICICI Bank Sapphiro Credit Card | 6,500 | 3,500 | Renewal fee waived on annual spends ≥ 6,00,000 | ~3.5% on foreign spends |

| YES Private Credit Card | 50,000 | 10,000 | Super–premium, invite-based; waiver as per bank | ~1.75% forex markup |

| ICICI Bank Emeralde Credit Card | 12,000 | 12,000 | Renewal waived on annual spends ≥ 10,00,000 | ~2.0% forex markup |

| IndusInd Pinnacle World Credit Card | 14,999 | 0 | One–time joining fee, no recurring annual fee | Standard (varies) |

| HSBC TravelOne Credit Card | 4,999 | 4,999 | Renewal waived on approx. annual spends ≥ 8,00,000 | Standard (around 3–3.5%) |

| IDFC FIRST Wealth Credit Card | 0 | 0 | Lifetime free, no waiver needed | ~1.5% forex markup |

| IndusInd Legend Credit Card | 5,000 | 0 | One–time joining fee, no annual fee | Discounted vs standard |

| SBI Card PRIME | 2,999 | 2,999 | Renewal fee waived on annual spends ≥ 3,00,000 | Typically ~3.5% |

| Axis Bank ATLAS Credit Card | 5,000 | 5,000 | Spend–based waiver as per the latest bank schedule | Typically standard range |

| AU Zenith Credit Card | 7,999 | 7,999 | Renewal waiver via high annual spend milestones | Lower-than-standard; Zenith+ at 0.99% |

| HDFC Regalia Gold Credit Card | 2,500 | 2,500 | Renewal waiver on crossing the bank’s annual spend slab | Often lower than basic cards |

| YES Bank Marquee Credit Card | 9,999 | 4,999 | Renewal waived on annual spends > 10,00,000 | ~1.0% forex markup |

How to Compare Travel Credit Cards (Checklist)

Comparing travel credit cards helps you find the one that best fits your travel patterns. The features can look similar at first glance, but each issuer prioritises a different benefit.

- Type of rewards: Choose between fixed airline miles and flexible travel points. Airline co-brands suit loyal flyers, while flexible points work for mixed-airline users.

- Reward rate: Check how many miles you earn per ₹100 or ₹150 spent on travel versus regular categories.

- Lounge access: Count both domestic and international visits allowed each year, and whether extra visits are chargeable.

- Foreign exchange markup: Compare markup fees on international spends and look for cards offering 2% or less.

- Welcome and milestone bonuses: Review how many bonus miles or vouchers you get on joining and on meeting spend targets.

- Airline or portal tie-ups: Verify if the card offers better value on a specific airline or booking website.

- Annual and joining fees: Check whether the fee is waived after a specified yearly spend.

- Travel insurance coverage: Note the coverage type (e.g., flight delay, lost baggage, or accident insurance) and its limit.

- Redemption flexibility: Check whether points can be redeemed for travel on multiple airlines or hotels, or only on a single partner.

- Reward expiry: Understand how long points remain valid and whether activity can extend them.

- Other privileges: Some cards add concierge services, hotel memberships, or free add-on cards.

Tips to Maximise Your Savings through Travel Credit Cards

A travel credit card can save a lot more when used strategically. A few small habits ensure you earn faster and lose fewer points along the way.

- Book flights through partners: Co-branded cards give higher mile value on their affiliated airline or portal. Booking elsewhere may cut earning rates.

- Meet milestone spends: Many issuers add bonus miles or vouchers after you reach set thresholds; plan bookings around those amounts.

- Redeem points early: Airline miles often expire within two or three years. Use them before expiry or transfer them to a partner to keep them active.

- Track lounge visits: Each card has a limited number of free entries. Keep count to avoid extra charges at the gate.

- Use the card abroad: Cards with low or zero forex markup, such as RBL World Safari or IDFC FIRST Wealth, give extra value on international payments.

- Avoid non-reward categories: Wallet loads, cash advances, and utility payments rarely earn travel points.

- Combine travel offers: Check for flight ticket credit card offers during sale seasons; stacking those with earned points gives better value.

- Pay statements on time: Late payments can cancel reward eligibility for that cycle and add interest charges that offset your savings.

Frequently Asked Questions (FAQs)

How do Travel Credit Cards earn rewards or air miles?

They award travel points or airline miles per ₹ spent, with higher earn rates on flights, hotels, and portal bookings. Co-branded cards credit miles to the partner airline; flexible cards bank points you can later transfer.

Can Travel Credit Cards be used for online and offline bookings?

Yes. You can pay on airline websites, OTAs, hotel portals, or at airport or hotel counters. Earn rates depend on card type and partner tie-ups.

Do Travel Credit Cards offer complimentary airport lounge access?

Most do. Access can be domestic-only on entry cards and both domestic + international on mid/premium cards. Free visits are capped per quarter or year.

Can Travel Credit Cards be used internationally?

Yes. They work worldwide where the network (Visa/Mastercard/Amex/Diners) is accepted. Good travel cards reduce foreign exchange (FX) markup; a few set it to 0%.

How do I redeem reward points or air miles?

Co-branded cards auto-credit miles to your airline account for ticketing or upgrades. Flexible points can be transferred to airline/hotel partners or redeemed for flights, hotels, or statement credit via the issuer portal.

Do Travel Credit Cards provide travel insurance?

Many include travel accident cover, trip delay/cancellation benefits, and lost baggage support. Limits and inclusions vary by issuer and card tier.

Can I hold multiple Travel Credit Cards?

You can. Frequent flyers often pair one airline co-brand with one flexible points card to balance fast earning with redemption options.

Are Travel Credit Cards suitable for first-time users?

Yes, entry-level variants work well if you fly a few times a year. Check annual fee, lounge limits, and reward expiry before choosing.

Can Travel Credit Cards convert purchases into EMI?

Most issuers allow high-value bookings to be converted to EMI in the app or on the statement. Interest and processing fees apply.

Most Popular on Urban Money

More Categories You Like

Travel Credit Cards from Other Banks