Top 10 Best Private Banks in India List 2025

January 09, 2025

February 03, 2023

In the latest update made by Finance Minister in the Union Budget 2024-25, Pradhan Mantri Awas Yojana received a major boost in fund assistance to 66%. This translates to the scheme receiving INR 79,000 Crores. Additionally, as per officials, Pradhan Mantri Awas Yojana, which was initially aimed at providing housing for all eligible individuals belonging to economically weaker sections of society by 2022, has now been extended to December 31, 2024. As a part of the mission, it is expected that the scheme is set to receive a boost in the upcoming union budget as well.

| Particulars | Details |

| New Update | Dates extended till December 31, 2024, |

| Official Website Link | https://pmaymis.gov.in/ |

| Launch Date | June 25, 2015 |

| Customer Care | Landline – 011-23063285, 011-23060484 Email – pmaymis-mhupa@gov[Dot]in |

The table below showcases the banks offering home loans under the PMAY Scheme.

| Name of the Bank | Interest Rate Applicable |

| State Bank of India (SBI) | 6.50% per annum |

| HDFC Ltd. | 6.50% per annum |

| LIC Housing Finance Ltd. | 6.50% per annum |

| ICICI Bank | 6.50% per annum |

| Axis Bank | 6.50% per annum |

| Bank of Baroda | 6.50% per annum |

| Canara Bank | 6.50% per annum |

| Union Bank of India | 6.50% per annum |

| PNB Housing Finance Ltd. | 6.50% per annum |

| DHFL (Dewan Housing Finance Corporation Ltd. | 6.50% per annum |

The steps below can be followed to take a home loan online under the PMAY scheme.

The steps below can be followed to take a home loan offline under the PMAY scheme.

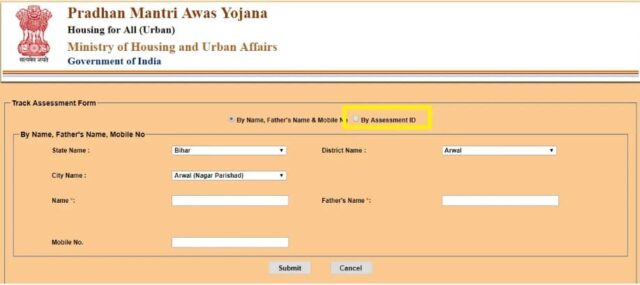

You can check the PMAY Application Status by following the steps listed below.

or

Note: You can also check your PMAY application status by visiting the official website of the Ministry of Housing and Urban Affairs (mhupa.gov.in) and following the same steps as above.

There are a few types of PMAY Schemes which are listed below.

The Pradhan Mantri Awas Yojana (PMAY) is a government scheme launched in 2015 to provide affordable housing to India’s urban and rural poor. The scheme has several features and benefits, including.

The beneficiaries of the PMAY scheme are listed below.

PMAY (Pradhan Mantri Awas Yojana) Interest Subsidy is a scheme launched by the Government of India to provide financial assistance to low and middle-income families to purchase or construct a house. Under this scheme, the government provides an interest subsidy on home loans taken by eligible beneficiaries. The interest subsidy is provided to eligible beneficiaries for 20 years or the loan tenure, whichever is lower. The scheme aims to provide affordable housing to all citizens and reduce the gap between the rich and the poor.

The table below pertains to the eligibility criteria for the PMAY Home Loan Scheme.

| Criteria | Description |

| Income | Household income should be less than or equal to Rs. 6 lakhs per annum. |

| Property | Should not own a pucca house either in their name or in the name of any family member in any part of India. |

| Family Size | Should be between 2 and 5 members. |

| Priority | Will be given to SC/ST, OBC, minorities, EWS, and LIG categories. |

| Age: | The female head of the household should be between 18 and 40 years old |

| Location | The house should be located in the country’s urban areas. |

| Construction | The house should be constructed for the first time. |

| Citizenship, | The applicant should be a citizen of India. |

| NOC | No Objection Certificate (NOC) from the concerned authority is required. |

When applying for a PMAY Home Loan scheme, you will be required to provide the following documents for authentication of identity, residence, and other particulars such as birth proof, declaration, and so on.

PMAY (Pradhan Mantri Awas Yojana) calculation is done to determine the eligibility and subsidy amount for the housing scheme. The analysis is based on the following factors:

The exact calculation of the PMAY subsidy amount can vary based on the scheme and the state in which it is being implemented. It is best to consult with a local housing authority or financial institution for more information.

The following are the main components of the PMAY scheme. These schemes are designed to cater to an array of economically-weaker sections of society. The particulars are as listed below.

Pradhan Mantri Awas Yojana (PMAY) is a housing scheme launched by the Indian government in 2015 to provide affordable housing to low and middle-income groups. The scheme has two components: Pradhan Mantri Awas Yojana – Urban (PMAY-U) and Pradhan Mantri Awas Yojana – Gramin (PMAY-G).

PMAY-U targets urban areas and aims to provide affordable housing to people who do not own a pucca house, with a focus on people belonging to economically weaker sections (EWS) and low-income groups (LIG). Under the scheme, the government provides financial assistance to eligible beneficiaries to construct or enhance a property. The assistance is provided as a subsidy on the home loan interest.

PMAY-G targets rural areas and aims to provide affordable housing to people living in rural areas who do not own a pucca house. Under the scheme, the government provides financial assistance to eligible beneficiaries to construct or renovate their property. The monetary aid is provided in the form of a subsidy on the home loan interest.

To be eligible for the scheme, beneficiaries must meet specific criteria such as income limits, land ownership, and citizenship. The scheme is implemented through partnerships between the Central and State governments and private and public sector entities.

The table provides the list of state-level nodal agencies for PMAY along with the organization’s name and address.

| State | Organization Name | Address |

| Andaman & Nicobar | Union Territory of Andaman and Nicobar Islands | Municipal Council, Port Blair – 744101 |

| Andhra Pradesh | Andhra Pradesh Township Infrastructure Development Corporation Limited | 502, Vijaya Lakshmi Residency, Gunadhala, Vijayawada – 520004 |

| Andhra Pradesh | Andhra Pradesh State Housing Corporation Limited | A.P.State Housing Corporation Ltd., Himayatnagar, Hyderabad – 500029 |

| Arunachal Pradesh | Government of Arunachal Pradesh | Department of Urban Development & Housing, Mob-II, Itanagar |

| Assam | Government of Assam | Block A, Room 219, Assam Secretariat, Dispur, Guwahati – 781006 |

| Bihar | Government of Bihar | Urban Development and Housing Department, Vikash Bhavan, Bailey Road, New Secretariat Patna |

| Chandigarh | Chandigarh Housing Board | Sec- 9-D, Chandigarh 160017 |

| Chattisgarh | Government of Chattisgarh | Room S-1/4, Mahanadi Bhawan, Mantralay Naya Raipur, Chhattisgarh |

| Dadra & Nagar Haveli and Daman & Diu | Union Territory of Dadra & Nagar Haveli | Secretariat, Silvassa – 396220 |

| Dadra & Nagar Haveli | Union Territory of Dadra & Nagar Haveli | Secretariat, Silvassa – 396220 |

| Goa | Government of Goa | GSUDA, 6th Floor, Shramshakti Bhavan, Patto- Panaji |

| Gujarat | Government of Gujarat | Affordable Housing Mission, New Sachivalya, Block No. 14/7, 7th floor, Gandhinagar – 382010 |

| Haryana | State Urban Development Agency | Bay -11-14, Palika Bhavan, Sector-4, Panchkula -134112 |

| Himachal Pradesh | Directorate of Urban Development | Palika Bhavan, Talland, Shimla |

| Jammu & Kashmir | J&K Housing Board | Housing Unit – 1, Channi Himmat, Sector – 2, Tawi Shopping Complex, J&K – 180015 |

| Jharkhand | Urban Development Department | 3rd floor, Room 326, FFP Building, Dhurwa, Ranchi, Jharkhand 834004 |

| Kerala | State Poverty Eradication Mission | TRIDA Building, Jn.Medical College P O Thiruvananthapuram |

| Madhya Pradesh | Urban Administration and Development, GoMP | Palika Bhawan, Shivaji nagar, Bhopal – 462016 |

| Maharashtra | Government of Maharashtra | Griha Nirman Bhawan, 4th Floor, Kalanagar, Bandra East – 400051 |

| Manipur | Government of Manipur | Town Planning Department, Government of Manipur, Directorate Complex, North AOC, Imphal-795001 |

| Meghalaya | Government of Meghalaya | Raitong Building, Meghalaya Civil Secretariat, Shillong – 793001 |

| Mizoram | Urban Development and Poverty Alleviation, Government. of Mizoram | Directorate of Urban Development and Poverty Alleviation, Thakthing Tlang, Aizawl, Mizoram, Pin: 796005 |

| Nagaland | Government. of Nagaland | Municipal Affairs Cell, A.G. Colony, Kohima – 797001 |

| Odisha | Housing and Urban Development Department | 1st Floor, State Secretariat, Annex – B, Bhubaneswar – 751001 |

| Puducherry | Government of Puducherry | Town and Country Planning Department. Jawahar Nagar Bomian Pet, Puducherry-605005 |

| Punjab | Punjab Urban Development Authority | PUDA Bhavan, Sector 62, SAS Nagar, Mohali, Punjab |

| Rajasthan | Rajasthan Urban Drinking Water, Sewerage & Infrastructure Corporation Limited | 4-SA-24, Jawahar Nagar, Jaipur, Rajasthan |

| Sikkim | Government of Sikkim | Department of UD & Housing, Government of Sikkim, NH 31A, Gangtok – 737102 |

| Tamilnadu | Government. of Tamilnadu | Tamil Nadu Slum Clearance Board, 5 Kamarajar Salai, Chennai – 600 005 |

| Telangana | Government of Telangana | Commissioner and Director of Municipal Administration, 3rd Floor, Ac Guards Public Health Lakdikapool Hyderabad |

| Tripura | Government of Tripura | Directorate Of Urban Development Government of Tripura Pt. Nehru Complex, Gorkha Basti, 3rd Floor, Khadya Bhawan, Agartala 799006 |

| Uttrakhand | Directorate of Urban Development | State Urban Development Authority 85A, Mothorawala Road Ajabpur Kalan – Dehradun |

| Karnataka | Government of Karnataka | 9th Floor Vishweshwaraih Towers, Dr Ambedkar Veedhi, Bangalore 560001 |

| West Bengal | State Urban Development Authority | ILGUS Bhaban, Block HC Block, Sector 3, Bidhannagar, Kolkata – 700106 |

| Uttar Pradesh | State Urban Development Agency (SUDA) | Navchetna Kendra, 10, Ashoka Marg, Lucknow 226002 |

The customer care helpline number for Pradhan Mantri Awas Yojana (PMAY) is 1800-11-6446.

| Related Resource |

| Home Loans For Women |

| Plot Loans for Land Purchase |

| Top Housing Finance Companies in India |

| Home Buying Tips |

| Top Home Loans |

PMAY or Pradhan Mantri Awas Yojana subsidy is a government scheme providing affordable housing loans for all economically weaker sections of the population, including the lower-income and middle-income groups.

Assessment ID for PMAY can be procured from the PMAY’s official portal. You must click the ‘search beneficiary’ option and enter your Aadhaar number. The assessment ID will be shown on the screen.

Can a female individual avail the PMAY benefits?

Senior citizens who are 60 and above have the provision to avail of the benefits of the Pradhan Mantri Vaya Vandana Yojana (PMVVY), a pension scheme with an assured return of 7.40% per annum.

DBT stands for Direct Benefit Transfer, in which the central assistance for the eligible applicants is directly transferred to their respective accounts.

Initially, the PMAY scheme was introduced to provide housing for all economically weaker sections of society by 2022. However, the mission has been extended until December 31, 2024.

CLSS or Credit Linked Subsidy Scheme is a provision for the PMAY beneficiaries from which they can procure financial assistance for purchasing, renovating, and maintaining their house.

December 10, 2025

June 18, 2025

April 03, 2025

March 25, 2025

March 25, 2025

March 24, 2025

Top 10 Best Private Banks in India List 2025

January 09, 2025

Top10 List of Petrol Pump Companies in India

January 09, 2025

Dairy Farm Loan in 2025 : Online Procedure

January 09, 2025

Top 10 Best Bank for Home Loan In India…

January 09, 2025

Top10 Best Student Credit Cards in India 2025

January 09, 2025

Products & Offers

Tools & Calculators

CIBIL Score

Credit Cards

© 2026 www.urbanmoney.com. All rights reserved.

Need Loan Assistance?