SBI Home Loan

SBI Home Loan has built a strong reputation based on trust, reliability, and customer satisfaction. One of the most appealing aspects of State Bank of India Home Loan is its competitive interest rates. SBI understands the significance of affordable EMIs (Equated Monthly Installments) for its customers. The SBI Home Loan product is not limited to a particular segment of the population. It caters to a wide range of individuals, including salaried employees, self-employed professionals, and even Non-Residential Indians (NRIs). This inclusivity ensures that everyone has the opportunity to achieve their homeownership goals with the support of State Bank of India. In addition, the bank’s simple documentation requirements make it easier for customers to finish their applications.

Unlock Best Home Loan Offers From State Bank Of India

State Bank of India Home Loan

Interest Rate

7.25% - 8.45%

Loan Amount

₹5L - ₹40Cr

EMI Per Lakh

₹1,992 - ₹2,049

Processing Fees

Pre-Payment Charges

--Plan Offered

Term Loan

Showing Data for CIBIL Score 800 - 1000

SBI Home Loans

CIBIL: 800 - 1000

CIBIL: 750 - 799

CIBIL: 700 - 749

View more

SBI Home Loans

CIBIL: 800 - 1000

View more

CIBIL Score range

CIBIL: 800 - 1000

CIBIL: 750 - 799

CIBIL: 700 - 749

CIBIL: 650 - 699

CIBIL: 550 - 649

CIBIL: 0 - 0

Showing Data for CIBIL Score 800 - 1000

- Salaried

- Self-Employed (Non-Professional)

- Self-Employed

| Loan Amount | Loan Type | Men (ROI) | Women (ROI) |

|---|---|---|---|

| Any Loan Amount | New | 8.65% | 8.60% |

- Salaried

- Self-Employed (Non-Professional)

- Self-Employed

| City | Loan Amount | Loan Type | Men (ROI) | Women (ROI) |

|---|---|---|---|---|

| Mumbai | Any Loan Amount | New | 8.65% | 8.60% |

Last updated on: 30, Mar 2026

Overdraft

Showing Data for CIBIL Score 800 - 1000

SBI Maxgain

CIBIL: 800 - 1000

CIBIL: 750 - 799

CIBIL: 700 - 749

View more

SBI Maxgain

CIBIL: 800 - 1000

View more

CIBIL Score range

CIBIL: 800 - 1000

CIBIL: 750 - 799

CIBIL: 700 - 749

CIBIL: 650 - 699

CIBIL: 550 - 649

CIBIL: 0 - 0

Showing Data for CIBIL Score 800 - 1000

- Salaried

- Self-Employed (Non-Professional)

- Self-Employed

| Loan Amount | Loan Type | Men (ROI) | Women (ROI) |

|---|---|---|---|

| Loans Above 20 Lacs | New | 9.10% | 9.05% |

- Salaried

- Self-Employed (Non-Professional)

- Self-Employed

| City | Loan Amount | Loan Type | Men (ROI) | Women (ROI) |

|---|---|---|---|---|

| Mumbai | Loans Above 20 Lacs | New | 9.10% | 9.05% |

| Pune | Loans Above 20 Lacs | New | 9.10% | 9.05% |

| Pimpri-Chinchwad | Loans Above 20 Lacs | New | 9.10% | 9.05% |

Last updated on: 30, Mar 2026

StepUp Loan

Showing Data for CIBIL Score 800 - 1000

SBI Flexipay

CIBIL: 800 - 1000

CIBIL: 750 - 799

CIBIL: 700 - 749

View more

SBI Flexipay

CIBIL: 800 - 1000

View more

CIBIL Score range

CIBIL: 800 - 1000

CIBIL: 750 - 799

CIBIL: 700 - 749

CIBIL: 650 - 699

CIBIL: 550 - 649

CIBIL: 0 - 0

Showing Data for CIBIL Score 800 - 1000

- Salaried

- Self-Employed (Non-Professional)

- Self-Employed

| Loan Amount | Loan Type | Men (ROI) | Women (ROI) |

|---|---|---|---|

| Loan Starts from 20 Lacs | New | 8.90% | 8.85% |

- Salaried

- Self-Employed (Non-Professional)

- Self-Employed

| City | Loan Amount | Loan Type | Men (ROI) | Women (ROI) |

|---|---|---|---|---|

| Mumbai | Loan Starts from 20 Lacs | New | 8.90% | 8.85% |

| Pune | Loan Starts from 20 Lacs | New | 8.90% | 8.85% |

| Kalyan-Dombivali | Loan Starts from 20 Lacs | New | 8.90% | 8.85% |

| Navi Mumbai | Loan Starts from 20 Lacs | New | 8.90% | 8.85% |

| Pimpri-Chinchwad | Loan Starts from 20 Lacs | New | 8.90% | 8.85% |

| Thane | Loan Starts from 20 Lacs | New | 8.90% | 8.85% |

| Vasai-Virar | Loan Starts from 20 Lacs | New | 8.90% | 8.85% |

Last updated on: 30, Mar 2026

Features & Benefits of SBI Home Loan

By choosing State Bank of India Home Loan, you can access an unmatched combination of features and benefits that prioritise your financial well-being, convenience, and long-term prosperity.

| Feature | Detail |

| Interest Rate | 8.40% – 10.15% p.a. |

| Loan Amount | Up to 90% of property value |

| Loan Tenure | Up to 30 years |

| Processing Charges | Up to ₹5,000* |

| Special Products | For defence personnel, government employees, non-salaried individuals, applicants buying ‘green’ homes, and individuals living in hilly/tribal areas. |

| Concessions | 0.05% interest rate concession for women borrowers |

| Additional Facilities | Home loan overdraft, balance transfer, top-up facility |

*T&C Applied

- Versatile Range of Home Loan Products: SBI offers an extensive array of home loan products meticulously designed to cater to the specific needs of every customer. Whether you are a first-time homebuyer, looking to renovate your existing property, or planning to purchase a plot of land, SBI has tailored solutions to suit your unique requirements.

- Highly Competitive Interest Rates: Experience the advantage of low-interest rates that make SBI Home Loans highly affordable. By securing a home loan from SBI, you can save significantly on interest payments over the loan tenure, making your homeownership journey more financially feasible and rewarding.

- Minimal Processing Fee: SBI believes in providing value to its customers from the beginning. With a minimal processing fee, SBI ensures that the costs of obtaining a home loan are kept low, allowing you to allocate more funds towards your dream home.

- Unwavering Transparency: Transparency is the cornerstone of SBI’s home loan offerings. Rest assured that there are no hidden charges or unpleasant surprises during the loan process. SBI is committed to maintaining complete transparency at every step, giving you peace of mind and confidence in your financial decisions.

- Flexible Prepayment Options:SBI understands the importance of financial freedom and offers the flexibility to make prepayments towards your home loan without incurring any penalty charges. This allows you to proactively manage your finances and accelerate your loan repayment, reducing the overall interest burden.

- Daily Reducing Balance Interest Calculation: State Bank of India home loans are structured with a daily reducing balance interest calculation methodology. This means that the interest charges on your home loan are recalculated on a daily basis, taking into account the principal amount you have repaid. As a result, you save more on interest costs and can repay your loan faster.

- Extended Repayment Tenure: SBI recognises that every borrower has unique financial circumstances. With an extended repayment tenure of up to 30 years, you can choose a tenure that aligns with your income and financial goals. This ensures that your monthly instalments are manageable and fit comfortably within your budget.

- Home Loan as an Overdraft: SBI goes beyond conventional offerings by providing the option to avail your housing loan as an overdraft facility. This unique feature empowers you to effectively manage your finances by utilising the loan amount whenever required while only paying interest on the utilised amount. It gives you the freedom to leverage your home loan for various financial needs without restrictions.

- Special Benefits for Women Borrowers: SBI recognises and appreciates the role of women in homeownership. As a gesture of support, SBI offers an interest concession to women borrowers, making housing loans more affordable and encouraging women to realise their dreams of owning a home.

State Bank of India Home Loans That Help You Achieve Your Goals

Choose Your Best SBI Home Loan

By Professions

By Property

By Other

SBI Home Loan Products or Schemes

State Bank of India offers a comprehensive range of home loan products designed to meet various needs, from purchasing new homes to constructing or renovating existing ones. Below, we explore the types of SBI home loans available to both resident Indians and NRIs, along with their key features.

SBI Regular Home Loan

- For: Indian Residents

- Purpose: Purchase a house, under-construction property, pre-owned homes, construction, repair, or renovation.

- Interest Rate: 7.20% – 8.35% for salaried; 8.20% – 8.50% for self-employed.

- Loan Tenure: Up to 30 years

- Processing Fee: 0.35% (min ₹2,000, max ₹10,000)

SBI NRI Home Loan

- For: NRIs or PIOs

- Purpose: Buying or investing in properties in India.

- Interest Rate: Varies

- Loan Tenure: Up to 30 years

- Processing Fee: 0.35% (min ₹2,000, max ₹10,000)

SBI Flexipay Home Loan

- For: Salaried, young earners

- Purpose: Allows for a higher loan amount with interest-only payments initially.

- Interest Rate: Varies

- Loan Tenure: Up to 30 years

- Processing Fee: 0.35% (min ₹2,000, max ₹10,000)

SBI Privilege Home Loan

- For: Government employees

- Purpose: Tailored for employees of Central & State Governments, including PSUs.

- Interest Rate: Varies

- Loan Tenure: Up to 30 years

- Processing Fee: Nil

SBI Shaurya Home Loan

- For: Defence personnel

- Purpose: Offers special benefits like attractive rates and zero processing fees.

- Interest Rate: Varies

- Loan Tenure: Up to 30 years

- Processing Fee: Nil

SBI Realty Home Loan

- For: Those purchasing plots for construction

- Purpose: Purchase of plot for construction within five years.

- Interest Rate: 8.90% – 9.10% based on loan amount

- Loan Tenure: Up to 10 years

- Processing Fee: 0.35% (min ₹2,000, max ₹10,000)

SBI Home Top-Up Loan

- For: Existing home loan borrowers needing additional funds

- Interest Rate: 8.60% – 10.65% based on loan amount

- Loan Tenure: Up to 30 years

- Processing Fee: 0.35% (min ₹2,000, max ₹10,000)

SBI Bridge Home Loan

- For: Homeowners upgrading to a new house

- Purpose: As the name implies, this loan bridges short-term liquidity between the sale and purchase of properties.

- Interest Rate: 10.35% first year, 11.60% second year

- Loan Tenure: Up to 2 years

- Processing Fee: 0.35% (min ₹2,000, max ₹10,000)

SBI Smart Home Top-up Loan

- For: General-purpose additional funding

- Interest Rate: 9.15% – 10.15% based on employment type

- Loan Tenure: Up to 20 years

- Processing Fee: ₹2,000 + GST

SBI Insta Home Top-up Loan

- For: Pre-selected customers via internet banking

- Interest Rate: 9.30%

- Loan Tenure: Min residual tenure of 5 years

- Processing Fee: ₹2,000 + GST

SBI Corporate Home Loan

- For: Public & Private Ltd organisations

- Purpose: Construction of residential units

- Interest Rate: Varies

- Processing Fee: 0.50% (min ₹50,000, max ₹10 lakh)

SBI Home Loan to Non-Salaried

- For: Non-Salaried Individuals

- Purpose: Construction, repair, renovation

- Interest Rate: Based on credit score

- Loan Tenure: Up to 30 years

- Processing Fee: 0.35% (min ₹2,000, max ₹10,000)

SBI Home Loan Schemes For You

State Bank of India Home Loan Fees and Charges

SBI home loan products come with a specific fee structure to ensure transparency and convenience for its customers. Here’s a breakdown of the fees and any additional charges associated with SBI’s home loan products:

Regular Home Loans and Other Home Loan Products

| Processing Fee | 0.35% of the loan amount, subject to GST. |

| Minimum Fee | ₹2,000, plus applicable GST. |

| Maximum Fee | ₹10,000, plus applicable GST. |

This fee structure applies to the Regular Home Loan and other specialised home loan products, including NRI, Realty, Maxgain, Corporate Real Estate (CRE), Flexi-pay, Non-salaried, Pre-approved Loan (PAL), Tribal Plus, and Apun Ghar loans for amounts above ₹15 lakhs.

Home Top-Up Loan

| Processing Fee | 0.35% of the loan amount, with applicable GST. |

| Minimum Fee | ₹2,000, plus applicable GST. |

| Maximum Fee | ₹10,000, plus applicable GST. |

This applies to additional funds borrowed on top of an existing home loan.

Personal Loan against Property (P-LAP)

| Processing Fee | 1% of the loan amount, plus applicable taxes. |

| Maximum Fee | ₹50,000, plus applicable taxes. |

For loans secured against the equity of the borrower’s property.

Digital Products: YONO Insta Home Top-Up, SMART Home Top-Up, and Insta Home Top-Up Loans

| Flat Fee | ₹2,000 plus GST for each product. |

They are designed for quick and easy online processing, offering additional funds to existing home loan customers.

Reverse Mortgage Loan

| Processing Fee | 0.50% of the loan amount, with applicable GST. |

| Minimum Fee | ₹2,000, plus applicable GST. |

| Maximum Fee | ₹10,000, plus applicable GST. |

A financial product for senior citizens that allows them to convert part of the equity in their home into cash.

Earnest Money Deposit (EMD) Scheme

| Processing Fee | 0.50%, applicable across the scheme. |

For customers participating in property auctions, offering them the convenience of loan support to manage earnest money deposits.

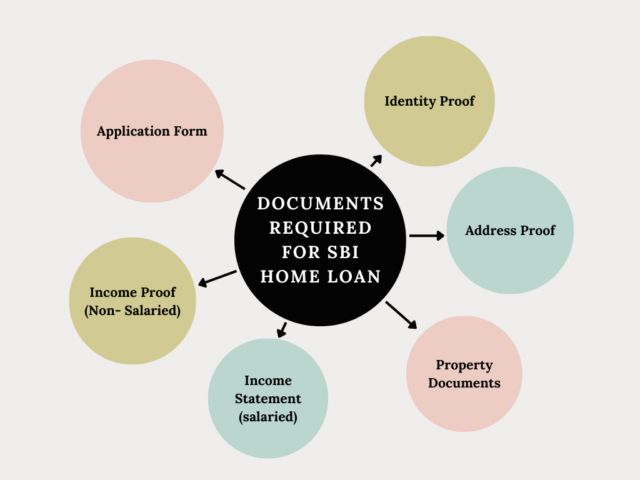

Documents Required for SBI Home Loan

To ensure a smooth and efficient housing loan application process, the State Bank of India (SBI) has streamlined the documentation requirements for their home loans. You can expedite the home loan approval process by providing the necessary documents and moving closer to realising your homeownership aspirations.

| Application form | Duly filled application form along with 3 passport-size photographs |

| Identity proof |

|

| Address proof |

|

| Property Documents |

|

| Income statement (salaried) |

|

| Income Proof (Non- Salaried) |

|

How Does the EMI Calculation Work for SBI Home Loan?

The EMI (Equated Monthly Instalment) calculation for an SBI housing loan follows a standard formula. Here’s how it works:

- Loan Amount: Determine the total home loan amount you borrow from SBI for your home purchase.

- Interest Rate: Check the prevailing SBI home loan interest rate offers. This rate may vary based on factors such as loan tenure, loan amount, and borrower’s credit profile.

- Loan Tenure: Decide on the duration or tenure of the loan, i.e., the number of years you will take to repay the housing loan.

- Calculation Formula: State Bank of India uses the reducing balance method to calculate EMIs, which means the interest is charged on the outstanding loan balance.

The formula used for EMI calculation is:

EMI = [P x R x (1+R)^N]/[(1+R)^N-1]

Where,

- EMI is the Equated Monthly Instalment.

- P is the loan principal amount.

- R is the monthly interest rate (annual interest rate divided by 12).

- N is the total number of monthly instalments (loan tenure in months).

With the help of SBI home loan EMI calculator, we have compiled a below mentioned table for your reference only,

| Home Loan Amount | ₹40,00,000 |

| Loan Tenure | 15 Years |

| Rate of Interest | 8.40% p.a* |

| Home Loan EMI | ₹39,155 |

| Interest Payable | ₹30,47,900 |

| Total Amount Payable | ₹70,47,900 |

Disclaimer: This above table is for your reference only. *Interest rates are subject to change timely.

Apply For SBI Home Loan upto 5 Crore and Calculate EMIs

Balance Transfer SBI Home Loan

Balance transfer of a home loan refers to the process of transferring an existing home loan from one lender to another, in this case, from a current lender to SBI (State Bank of India). It can benefit borrowers if they obtain a lower interest rate or better terms with the new lender.

If you are considering a balance transfer of your home loan to SBI, here are the key steps involved:

- Evaluate your current home loan: Assess your existing home loan terms, including the interest rate, tenure, outstanding balance, and any applicable charges or penalties for prepayment or foreclosure.

- Research SBI home loan offers: Explore the various home loan products offered by State Bank of India and compare them with your current loan. Pay attention to the interest rates, processing fees, loan tenure, and other terms and conditions.

- Calculate potential savings: Use an online home loan balance transfer calculator or consult with SBI to determine the potential savings you can achieve by transferring your home loan. Consider factors such as lower interest rates, reduced EMIs, and overall cost savings over the loan tenure.

- Gather required documents: Prepare the necessary documents required for the balance transfer application. These may include identity proof, address proof, income documents, property documents, and any other documents specific to SBI’s requirements.

- Submit application and documentation: Visit the nearest SBI branch or apply online to initiate the balance transfer process. Complete the application form and submit the required documents as per SBI’s guidelines.

- Verification and approval: State Bank of India will verify your application and documents. They may conduct a credit appraisal and property valuation as part of the process. If all requirements are met, and your application is approved, SBI will issue a sanction letter for the balance transfer.

- Loan closure with existing lender: Once the balance transfer is approved, coordinate with your existing lender to close the current home loan account. Ensure that all outstanding dues, foreclosure charges, and necessary paperwork are completed as per their procedures.

- Loan disbursement with SBI: After the closure of the previous loan, SBI will disburse the loan amount to your account or as agreed upon in the sanction letter. The outstanding amount from your previous loan will be transferred to your new SBI home loan account.

Apply Home Loan in Your City

FAQs

From loans to affordable interest rates, we have the answers for everything you need to know.

How to Obtain a Home Loan from SBI?

You can apply for an SBI home loan directly through Urban Money. The entire process, from checking eligibility to submitting documents, takes place online. Urban Money assists in comparing loan offers, providing support with paperwork, and tracking the application at every stage.

Is property insurance mandatory for an SBI home loan?

SBI does ask for property insurance when a home loan is availed. It’s not something the RBI makes compulsory, but banks usually include it to cover risks such as fire, structural damage, or natural disasters. This is primarily to protect both the borrower and the bank if anything goes wrong with the property.

What is the drawing power of the SBI home loan?

Drawing power is the limit on how much can be withdrawn from the sanctioned loan. It’s based on factors such as current property value, repayment history, and overall creditworthiness. The amount can also decrease over time if part of the loan has already been repaid or prepayments have been made.

What are the documents required for a home loan in SBI?

The paperwork typically includes a combination of identity, income, and property-related documents. A variety of identity, income, and property-related papers are often included in the documentation. This includes documents such as a current utility bill or passport to prove residence, Aadhaar or PAN to prove identity, and pay stubs or bank statements to prove income. SBI also requires a completed application form and passport-sized photos to accompany it.

What is the moratorium period in the SBI home loan?

The moratorium period is a phase where only interest is paid; the EMI doesn’t cover the principal yet. It often comes into play at the start of the loan or in special schemes, such as FlexiPay, which can offer this buffer for a few years. In certain cases, such as financial strain, SBI may extend this period through restructuring.

What is an overdraft facility in the SBI home loan?

SBI’s Maxgain scheme works like an overdraft linked to the home loan. EMIs are paid as usual, but the account also lets borrowers park extra money. That surplus helps lower the interest burden and can be reinvested if needed. The available limit decreases each month as the loan is repaid.

How to Transfer an Existing Home Loan to SBI?

This can be done online through Urban Money or by visiting an SBI branch. After applying, the bank checks the paperwork and contacts the existing lender to close the old loan. Once that’s cleared, the new loan starts under SBI’s structure.

How much home loan can I get from SBI?

It depends on several factors, mainly income, current monthly expenses, and the property’s value. SBI also follows the LTV norms set by the RBI, which means the buyer must cover part of the cost, and the rest can be financed if their profile qualifies.

What is the processing fee for an SBI home loan?

The processing cost that SBI levies is 0.35% of the loan amount. The exact figure may shift slightly depending on the loan type or scheme being used. The lowest processing fee is ₹2,000, whereas the highest is ₹10,000, inclusive of GST.

Can I reduce the home loan tenure in SBI?

Yes, the tenure can be reduced by making part-payments or clearing a larger amount ahead of time. This reduces the overall interest paid, as the loan is repaid sooner.

How to calculate home loan eligibility in SBI?

SBI’s online calculator checks eligibility using income, age, ongoing liabilities, and how much the property is worth. It also provides a rough EMI comparison side by side, which helps in planning the loan amount more effectively.

How to do prepayment of an SBI home loan?

Prepayments can be done through net banking, the YONO app, or directly at the branch. If it’s a floating-rate loan, there’s no penalty, whether it’s a part-payment or clearing the whole thing.

How to reduce EMI in an SBI home loan?

EMIs can be reduced in several ways, by switching to a lower interest rate, increasing the loan tenure, or making a part payment to reduce the principal. Some borrowers also shift between fixed and floating rates depending on what works better.

Is a guarantor required for an SBI home loan?

In most cases, no. If the credit profile and income are strong, SBI typically doesn’t require a guarantor. However, for higher loan amounts or slightly riskier profiles, a co-applicant or guarantor may be added for additional support.

What is LTV in an SBI home loan?

LTV refers to the percentage of the property’s cost that the bank will finance. It usually ranges from 75% to 90%, based on the property value and RBI’s rules. The rest needs to come from the borrower.

What is MCLR in the SBI home loan?

MCLR was the older method SBI used to price home loans. These days, they are referred to as something called RLLR — a rate that changes in response to the RBI’s adjustments to the repo rate. So, MCLR is no longer active.

Does SBI check CIBIL for a home loan?

Yes, SBI reviews the credit score when evaluating any home loan application. A strong score, somewhere in the 700 range or higher, usually makes the process smoother. It may help you secure a better interest rate, depending on your profile.

Does the SBI home loan include stamp duty registration?

No, costs like stamp duty, registration charges, and legal or valuation fees aren’t included in the loan amount. These need to be paid separately by the borrower at the time of property registration.

How much time does SBI take to process a home loan?

Typically, it takes about a week, sometimes a little longer or shorter, if all the paperwork is complete and the property check goes smoothly. However, delays can happen if there is missing information or if something needs to be reviewed again. In more complicated cases, a few weeks is common.

What are the benefits SBI provides on a home loan?

SBI provides attractive interest rates, occasionally offering slight concessions for women borrowers. There are no prepayment penalties on floating-rate loans, and products like Maxgain enable flexible repayment options with overdraft features. The entire process can be done digitally, from verifying eligibility to monitoring EMIs.

How do I transfer my existing home loan to the State Bank of India?

This works similarly to a balance transfer. Apply through Urban Money or an SBI branch, submit the details of the existing loan, and once it’s approved, SBI will close the old loan with the current lender and shift the balance to their terms.

Quick Links

Loan Offers By State Bank Of India's

Home Loan by Nationalized Bank

Home Loan by Private Bank

- Reliance Capital Home Loan

- YES Bank Home Loan

- RBL Bank Home Loan

- IDFC FIRST Bank Home Loan

- DCB Bank Home Loan

- Federal Bank Home Loan

- ICICI Bank Home Loan

- karur Vysya Bank Home Loan

- Axis Bank Home Loan

- CITI Bank Home Loan

- HDFC Bank Home Loan

- Housing Development Finance Corporation Home Loan

- HDFC Sales Home Loan

- Kotak Bank Home Loan

- IndusInd Bank Home Loan

- LIC Housing Finance Home Loan

- HSBC Home Loan

- IDBI Bank Home Loan

- karnataka bank Home Loan

Home Loan by NBFC

- Clix Capital Home Loan

- Vastu Housing Finance Home Loan

- Aadhar housing Finance Home Loan

- Hero FinCorp Home Loan

- Muthoot Finance Ltd Home Loan

- Edelweiss Financial Services Home Loan

- Cholamandalam Finance Home Loan

- Piramal Finance Home Loan

- SMFG India Credit Company Ltd Home Loan

- Ujjivan Small Finance Bank Home Loan

- Capri Global Home Loan

- Hero Housing Finance Home Loan

- Poonawalla Fincorp Limited Home Loan

- Capital First Ltd. Home Loan

- IndiaBulls Home Loan

- IIFL Finance Home Loan

- L&T Finance Home Loan

- DHFL Home Loan

- Tata Capital Housing Finance Limited Home Loan

- Home First Finance Company Home Loan

- Punjab National Bank Housing Finance Home Loan

- Godrej Housing Finance Home Loan

- Aditya Birla Finance Limited Home Loan

- Bajaj Finserv Home Loan

Home Loan Calculators

Latest from the Home Loan Blog

Get in-depth knowledge about all things related to Home Loan and your finances

Home Loan Interest Rates Cut 2025: RBI Repo Move Triggers Big Rate Reductions Across 6 Major Banks

Following the RBI’s 5 December repo rate cut to 5.25%, six major banks have begun trimming home loan benchmarks, so borrowers may soon see lower interest rates on floating-rate loans and lighter EMIs

Top 5 Legal Documents You Need for a Hassle-Free Home Loan Process

Getting a home loan can be smooth if you have all the right documents. Lenders need certain legal documents for a home loan to verify your identity, income, and property details. Having these ready in

Home Loan Exemptions : Tax Rebates, High Savings

A home loan can not only get you your dream home —it can also help you save on taxes! Home loan exemptions offered by the Income Tax Act (1961) allow borrowers to claim rebates that lower their taxabl

Home Loan Disbursement Process For Under Construction Property

Investing in under-construction properties offers affordability and long-term benefits. It is a popular choice among homebuyers. These properties provide flexible payment plans and potential appreciat

Understanding Principal and Interest – An Introduction

Money makes the world go round, but borrowing it can sometimes feel like a puzzle. When you take a loan, you hear words like “principal” and “interest” tossed around, but what do they actually mean? T