- Home

- Home Loan

- Tata Capital Housing Finance Limited

- Tata Capital Home Loan Eligibility Calculator

Tata Capital Home Loan Eligibility Calculator

The Tata Capital Home Loan Eligibility Calculator is an online digital tool designed to help potential home buyers quickly gauge the loan amount they might be eligible to borrow based on their financial details. By inputting various parameters like monthly income, monthly expenses, existing monthly loan repayments, desired loan tenure, and the applicable rate of interest (often pre-filled based on Tata Capital’s current offerings), users can obtain an estimate of the loan amount they might be qualified for.

- Personalized Home Loan solutions

- Expert guidance

- Application assistance

- Credit score discussion

- Home Loan Interest rate comparison

Table of Content

Last Updated: 11 March 2026

Tata Capital Home Loan Eligibility Calculator – Key Features & Benefits

Following are the benefits of using Tata Capital Home Loan Eligibility Calculator:

- User-Friendly Interface: The calculator is typically designed with a straightforward interface, making it easy for users to enter their financial details.

- Multiple Input Parameters: The calculator allows users to input various financial details such as:

- Monthly income

- Monthly expenses

- Existing monthly loan repayments

- Desired loan tenure

- Rate of interest (which might be pre-filled based on current rates offered by Tata Capital)

- Instant Results: Once the details are entered, the calculator quickly processes the data to provide an estimated loan amount that a user might be eligible for.

- Online Access: Being a digital tool, it can be accessed anytime and anywhere, providing flexibility to users.

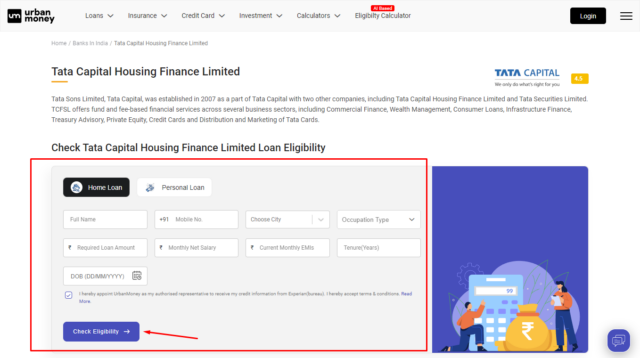

How to use Tata Capital Home Loan Eligibility Calculator?

Here’s how you can use Tata Capital Home Loan eligibility calculator:

- Log on to www.urbanmoney.com

- Select ‘Home Loan’ from the ‘Loans’ category.

- Choose ‘Tata Capital’ from the wide range of home loan providers.

- The portal will lead you to the ‘Tata Capital Home Loan’ page.

- Enter the required information and accept the T&Cs.

- Click on ‘Check Eligibility.’

- Enter the OTP sent to your mobile number and get instant eligibility results.

The Urban Money calculator offers the estimated loan amount a candidate is eligible for, along with the applicable interest rate, tenure and EMI estimates. Click ‘Apply now’ to proceed with the offer, or select ‘View All Offers’ to surf through other options.

Tata Capital Home Loan Eligibility Criteria

Customers require home loans for different purposes. Indian bank offers a variety of home loans to the following candidates:

- Salaried Employees

- Self-Employed Individuals

- Pensioners

- Indian Bank staff and their spouses

- NRIs

- Existing Home Loan borrowers

Tata Capital Home Loan Eligibility Based on Salary

- Higher Salary, Higher Loan Amount: Generally, the higher your salary, the more you’re deemed capable of repaying a larger loan amount. Lenders perceive individuals with a substantial salary as low-risk borrowers.

- Debt-to-Income Ratio: It’s not just the gross salary that Tata Capital considers but also the portion of the salary that is already committed to other debts. The lesser your existing liabilities, the higher the amount you might be eligible for.

- Stability of Income: Besides the amount, the consistency and stability of one’s salary play a role. Regular income from a stable job or long-running business can improve loan eligibility.

- Savings and Expenditures: Your net savings after all monthly expenses can influence the loan amount. The more you save, the more confidence Tata Capital has in your ability to handle EMIs.

- Salary Slips and Bank Statements: As a standard procedure, Tata Capital would require recent salary slips and bank statements as proof of income. These documents serve as validation of your declared income.

- Joint Application: If your salary alone doesn’t qualify you for the desired loan amount, consider applying jointly, perhaps with a spouse or a family member. Combined salaries can substantially increase your loan eligibility.

- Fixed vs. Variable Salary: For those earning a variable salary (like incentives, or bonuses), Tata Capital might consider an average of your earnings over a specific period to determine the eligible loan amount.

Tata Capital Home Loan Eligibility Criteria for Self-Employed Individuals

- Business Stability: Tata Capital will evaluate the number of years you’ve been in business. A longer, consistent business history often translates to a higher likelihood of loan approval.

- Proof of Income: Unlike salaried individuals, self-employed applicants might need to provide:

- Recent Income Tax Returns (usually for the last 2-3 years).

- Profit and Loss statements and balance sheets certified by a chartered accountant.

- Bank statements showcasing business transactions.

- Debt-to-Income Ratio: Just like their salaried counterparts, self-employed individuals need to ensure that a significant portion of their income isn’t already tied up with other debts. A healthy balance between income and existing obligations is vital.

- Credit Score: A robust credit score is crucial. It indicates financial responsibility and can boost your chances of loan approval. Timely payment of business loans or credit card bills will reflect positively on your credit history.

- Nature of Business: Some sectors or industries might be deemed riskier than others. Tata Capital may take into account the nature of your business and its market reputation when determining loan eligibility.

- Age: While age is a common factor for all borrowers, for self-employed individuals, it may also relate to the lifecycle of the business. Young entrepreneurs might be evaluated differently than those with well-established ventures.

- Savings and Investments: Evidence of savings, investments, or assets can act as a testament to financial stability and can positively influence loan eligibility.

Tata Capital NRI Home Loan Eligibility: Requirements for Non-Resident Indians

Non-Resident Indians (NRIs) form a substantial part of the global diaspora, and many look to invest in properties back home in India. Recognizing this demand, Tata Capital offers specialised home loan products tailored for NRIs. If you’re an NRI considering purchasing property in India, here’s what you need to know about Tata Capital’s eligibility criteria:

- Residency Status: The borrower must have a valid Indian passport along with an NRI status. Along with this, people of Indian origin must also be eligible, however, they must adhere to a slightly different documentation requirement.

- Employment Stability: Tata Capital typically requires NRIs to have a minimum employment period in their current job abroad. This can vary but is generally around 2 years of work experience in the country of residence.

- Income Criteria: The minimum salary or income requirement might differ based on the country of residence. It’s essential to verify the specific criteria for your residing country.

- Valid Work Permit/Visa: A valid work permit or visa in the country of residence is a must. Some lenders might also look into the visa’s validity duration to ensure stability.

- Creditworthiness: Even if you’re residing abroad, a good credit score or credit history in your country of residence can influence your loan eligibility. Some lenders also refer to credit reports from India, if available.

- Age Limit: There’s usually an age criterion, both minimum and maximum, by the time of loan maturity. This ensures that the borrower has a stable income during the entire loan tenure.

Special Tata Capital Home Loan Eligibility for Women Applicants

Empowering women in the realm of homeownership has been a priority for various financial institutions, including Tata Capital. They offer tailored home loan packages with potentially favourable terms for women applicants, recognizing their unique socio-economic contributions and challenges. Here’s a closer look at Tata Capital’s home loan eligibility criteria for women:

- Applicant Status: While women can apply as sole applicants, they can also apply as co-applicants along with other family members. This can enhance loan eligibility, especially if the woman is a primary or equal breadwinner in the family.

- Special Interest Rates: Financial institutions, including Tata Capital, sometimes offer reduced interest rates for women applicants as an incentive to boost female homeownership.

- Employment and Income: Whether a woman is salaried or self-employed, Tata Capital will evaluate her monthly/annual income, employment or business stability, and the continuity of income. This is similar to other applicants but ensures that the woman’s financial capabilities are independently assessed.

- Credit Score: A good credit score is crucial. Regular and timely payment of credit card bills, previous loans, and other financial commitments can enhance loan eligibility.

- Age Criteria: There’s typically an age bracket (minimum and maximum) to ensure that the applicant can repay the loan comfortably within the chosen tenure.

- Existing Liabilities: Any existing debts or monthly obligations will be considered to determine the applicant’s capacity to manage additional loan EMIs.

- Documentation: Standard documentation like identity proof, address proof, income proof, property details, and others will be needed. However, the exact documents might vary depending on whether the woman is salaried or self-employed.

List of Factors Affecting Tata Capital Home Loan Eligibility

Here is the list of factors that affect the Tata Capital Home Loan Eligibility:

- Age: It is one of the most important factors that helps in determining the eligibility for a housing loan. As a home loan has to be paid in the long term, the repayment is calculated based on the age of the working individual. Because of this, the younger you are the more preference will be given to you.

- Level of Income: Based on the nature of the employment and one’s profession, banks and other financial institutions consider giving out loans to the borrowers. Thus, having a steady source of income also matters when you apply for a home loan. The higher the income, the higher the loan amount banks and other lenders will be ready to offer you.

- Credit Score: Before any lender or a bank approves the loan, they try to gauge and evaluate the repayment ability of the borrower in the form of a credit score. For the unversed, a credit score accounts for multiple aspects of one’s credit profile like repayment history, the types of loans borrowed in the past, along with any existing credit card dues. Thus, it becomes very crucial to maintain a credit score of 750 or above.

How Can You Improve Your Tata Capital Home Loan Eligibility?

Here’s how you can improve your Tata Capital Home Loan eligibility:

- Increase Income Sources: More sources of income means higher loan eligibility.

- Clear Existing Loans: If you have any existing loans then one of the best ways to improve your home loan eligibility would be to clear all your existing debts.

- Check Credit Score: A higher credit score not only improves eligibility but can also help in securing loans at more favourable interest rates. Always pay your EMIs and credit card dues on time.

- Opt for Longer Tenure: Choosing a longer loan tenure might increase the amount you’re eligible for, but remember, this means you’ll be paying interest for a longer period.

- Joint Application: Applying for a home loan with a co-applicant (like a spouse with a steady income) can significantly increase your loan eligibility.

- Avoid Multiple Applications: Every loan application results in a credit check. Multiple checks in a short span can reduce your credit score. Only apply after thorough research.

- Keep Records Handy: Proper documentation, such as proof of income, tax returns, and bank statements, can expedite the loan approval process and can sometimes impact the amount you’re eligible for.

- Check Property Details: The property you intend to buy should not have legal issues. Banks may reject loan applications or reduce the eligible amount if the property doesn’t meet their criteria.

Understanding Impact of Credit Score on Tata Capital Home Loan Eligibility

Credit score has a substantial impact on home loan eligibility. The following points must be considered for understanding the impact of credit score on Tata Capital Home Loan eligibility.

- Interest Rates: A high credit score can help you secure a loan at a lower interest rate. Lenders perceive those with higher scores as low-risk borrowers and may offer them preferential interest rates. Conversely, a lower credit score might lead to higher interest rates or even loan denial.

- Loan Amount: Your credit score can influence the maximum loan amount you’re eligible for. A high score can boost your chances of getting a higher loan amount because it signifies better financial discipline and reliability.

- Loan Tenure: While credit score primarily affects the rate of interest and loan amount, in some cases, it might influence the loan tenure. A good credit score might provide more flexibility in choosing a longer repayment period.

- Loan Approval: A credit score below the lender’s threshold can lead to outright rejection of the loan application. On the other hand, a high credit score can expedite the loan approval process.

- Additional Charges: Those with lower credit scores might have to pay higher processing fees or other additional charges. Some lenders might waive or reduce these charges for borrowers with exceptional credit scores.

- Joint Loan Impact: If you’re applying for a joint home loan and one of the applicants has a poor credit score, it can affect the overall eligibility of the loan. In such cases, it’s beneficial if the primary applicant has a stronger credit score.

Comparing Eligibility Across Different Tata Capital Home Loan Products

Product/Criteria |

Loan Amount |

Loan Tenure |

Interest Rate Starting |

| Home Loans | 5 lakh to 5 crores | Up to 30 years | 8.70%* p.a. |

| Loans Against Property | 5 lakh to 5 crores | 12-240 months | 10.10%* pa.a |

| Affordable Housing Loan | 2 lakh onwards | Up to 30 years | 10.10%* pa.a |

| Home loan for government employees | 5 lakh to 5 crores | Up to 30 years | 8.70%* p.a. |

| Home loan for self-employed | 5 lakh to 5 crores | Up to 30 years | 8.70%* p.a. |

| Home loan for women | 5 lakh to 5 crores | Up to 30 years | 8.70%* p.a. |

People Also Asked About Tata Capital Home Loan Eligibility Calculator

How to check Tata Capital home loan eligibility without difficulty?

To check your Tata Capital home loan eligibility, you can visit the official website of Tata Capital where you can check your eligibility on the Tata home loan eligibility calculator. You can also check your home eligibility via www.urbanmoney.com

How much loan am I eligible for Tata Capital?

The exact home loan amount for which you as a borrower are eligible will depend on multiple factors such as monthly expenses, existing financial commitments and the borrower’s credit history. To determine the exact amount, you can get a basic estimate of the total loan amount.

How will I know if my eligibility criteria have been met for Tata Capital home loans?

As you apply for a Tata Capital Home Loan, they will conduct a thorough assessment of your financial health as a borrower. Once the evaluation is done, a Tata Capital representative will get in touch with you to inform you about your eligibility.

How can I increase my eligibility for a higher Tata Capital home loan amount?

To do this, you can consider increasing your overall income, cutting back on your existing liabilities, maintaining a good credit score, opting for a longer loan tenure, and applying for a loan with a co-applicant.

Quick Links

Loan Offers By Tata Capital Housing Finance Limited's

Home Loan Calculators

Tata Capital Housing Finance Limited Calculators

Bank wise Home Loan Calculators

- Axis Bank Home Loan Calculator

- Canara Bank Home Loan Calculator

- Idfc First Bank Home Loan Calculator

- Hsbc Home Loan Calculator

- Indusind Bank Home Loan Calculator

- Hdfc Bank Home Loan Calculator

- Kotak Bank Home Loan Calculator

- State Bank Of India Home Loan Calculator

- Aditya Birla Finance Limited Home Loan Calculator

- Idbi Bank Home Loan Calculator

- Iifl Finance Home Loan Calculator

- Karur Vysya Bank Home Loan Calculator

- Piramal Finance Home Loan Calculator

- Tata Capital Housing Finance Limited Home Loan Calculator

- Union Bank Of India Home Loan Calculator

- Punjab National Bank Home Loan Calculator

- Bank Of India Home Loan Calculator

- Bank Of Baroda Home Loan Calculator

- Lic Housing Finance Home Loan Calculator

- Punjab Sind Bank Home Loan Calculator

- Indian Bank Home Loan Calculator

- Bank Of Maharashtra Home Loan Calculator

- Citi Bank Home Loan Calculator

- Rbl Bank Home Loan Calculator

- Karnataka Bank Home Loan Calculator

- Federal Bank Home Loan Calculator

- Deutsche Bank Home Loan Calculator

- Yes Bank Home Loan Calculator

- Icici Bank Home Loan Calculator