- Home

- Personal Loan

- Punjab National Bank

- PNB Personal Loan Eligibility Calculator

PNB Personal Loan Eligibility Calculator

The PNB Personal Loan Eligibility Calculator is a tool designed to determine the EMIs that need to be repaid. All one needs to do is put in the basic information, such as monthly income, existing liabilities, age, employment status, etc. It won’t be an understatement to say that the PNB’s Personal Loan Eligibility Calculator acts as a valuable resource for those considering a personal loan from the institution.

- Personalized Personal Loan solutions

- Expert guidance

- Application assistance

- Credit score discussion

- Personal Loan Interest rate comparison

Last Updated: 28 March 2026

PNB Personal Loan Eligibility Calculator – Key Features & Benefits

Here are the key features and benefits of the PNB Personal Loan Eligibility Calculator.

- With PNB personal loan eligibility calculator, you can expect immediate results that will further streamline your decision-making process.

- Designed with simplicity in mind, the PNB personal loan calculator ensures that even those with minimal technical expertise can navigate and use the tool with ease.

- Based on the details provided by the user and in alignment with PNB’s lending criteria, the PNB Personal loan calculator offers accurate estimations of eligible loan amounts.

- Users can be assured that their personal and financial details are kept confidential and are used solely for the purpose of calculating loan eligibility.

- The tool is available for free on PNB’s website, and users are under no obligation to apply for a loan just because they’ve used the calculator.

- By getting an idea of their borrowing capacity, users can make informed financial decisions and plan their borrowing better.

- Available online, the PNB Personal Loan Eligibility Calculator can be accessed at any time, offering convenience to users regardless of their schedules.

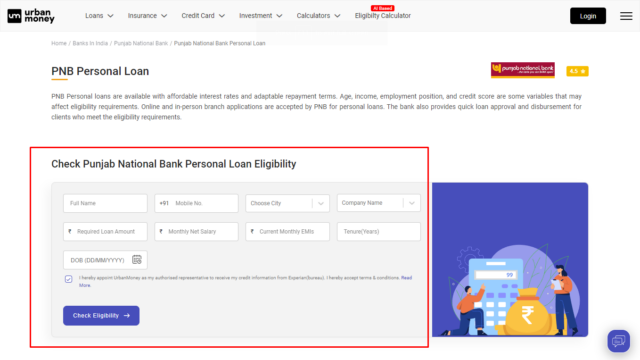

How to use Punjab National Bank Personal Loan Eligibility Calculator?

Urban Money offers an easy to use Punjab National Bank personal loan eligibility calculator in these simple steps:

- Log on to www.urbanmoney.com

- Select ‘Personal Loan’ from the ‘Loans’ category.

- Choose ‘Punjab National Bank’ from the available banks and NBFCs list.

- The portal will direct you to the ‘PNB Personal Loan’ page.

- Fill in the required details and accept the terms and conditions.

- Click on ‘Check Eligibility’.

- Complete the OTP verification and get instant estimates.

The PNB personal loan calculator also provides loan terms like interest rates, loan tenure, EMI payments, and the estimated personal loan amount. Click ‘Apply Now to apply for the loan, or select ‘View All Offers’ to browse through other options.

Punjab National Bank Personal Loan Eligibility Criteria

Here is a basic snapshot of the Punjab National Bank eligibility criteria for availing a personal loan.

- Applicant Profile: Personal loans from PNB are typically available to salaried individuals, self-employed professionals, and businessmen.

- Age: Borrowers usually need to be within a certain age bracket. For example, they might need to be above 21 years old and below 60 years old at the time of loan maturity, though the exact age range can vary.

- Employment Stability: For salaried individuals, a minimum period of employment, often a year or more with the current employer, might be necessary. Self-employed individuals or businessmen might need to show a minimum number of operational years in their current profession or business.

- Minimum Income: There’s typically a minimum monthly or annual income requirement to ensure that the borrower can repay the loan. This amount might vary based on the city or region, given the differences in the cost of living.

- Credit Score: A good credit history and a satisfactory credit score are vital. While the exact score might vary, a higher credit score can increase the chances of loan approval and might even fetch better interest rates.

- Existing Liabilities: Your current debts and liabilities will be considered. The bank will assess if you can handle the additional EMI burden given your current financial obligations.

- Residential Status: Some banks, including PNB, might have a preference for applicants who have been residing at their current address for a certain number of years.

- Documentation: Proper and verifiable documentation is essential. This includes identity proofs, income proofs, residence proofs, and others that the bank might deem necessary.

Punjab National Bank Personal Loan Eligibility Based on Salary

Here’s the Punjab National Bank Personal Loan Eligibility based on salary.

- Minimum Monthly Income: PNB will typically set a minimum monthly income requirement for personal loan applicants. This threshold ensures that the borrower has a stable income source to meet the monthly installment payments. The exact amount might vary based on the city of residence since urban areas might have a higher threshold due to a higher cost of living. For instance, doctors should earn a minimum salary of 5 lakh or above.

- Employment Duration: Alongside the salary, the length of time one has been employed with the current employer might also be considered. A stable employment history can be a positive indicator of one’s financial stability. Usually, the employee should be there with his/her respective company for 2 years.

- Annual Bonus or Incentives: Apart from the basic salary, regular bonuses or incentives might also be factored into the eligibility calculation, provided they can be substantiated with documentary proof.

- Nature of Employment: Permanent employees might have an edge over temporary or contractual employees since they represent a more stable income source.

Punjab National Bank Personal Loan Eligibility Criteria for Self-Employed Individuals

For self-employed individuals seeking a personal loan from Punjab National Bank (PNB), the eligibility criteria can differ slightly from those of salaried individuals due to the nature of their income and business stability. Here are the typical criteria PNB might consider for self-employed applicants:

Punjab National Bank Personal Loan Eligibility Criteria for Self-Employed Individuals:

- Business Continuity: One of the foremost criteria is the number of years the business has been operational. PNB typically requires that the business be operational for a minimum number of years, which ensures stability and reliability of income.

- Annual Profit or Turnover: The bank will look into the annual profit or turnover of the business. A consistent and growing profit indicates a healthy business, making the individual a reliable borrower.

- Proof of Business: Relevant documents such as a business licence, GST registration, partnership deeds (if applicable), or any other certifications that validate the existence and legitimacy of the business are necessary.

- Income Tax Returns: PNB will likely require self-employed applicants to submit their Income Tax Returns (ITRs) for the last few years. This not only validates the declared income but also shows the financial health of the business.

- Credit Score: Just like with salaried individuals, a good credit score is vital for self-employed individuals. This score, derived from past credit behaviour, gives the bank an idea of the borrower’s creditworthiness.

- Nature of Business: Some banks might have preferences for certain business types over others based on perceived risks associated with different industries.

- Business Stability: Factors like the presence of recurring clients, contracts in hand, and overall market reputation can play a role in determining eligibility.

- Bank Statements: The bank statements of the business for the past months or years can provide insights into the cash flow and financial health of the business.

- Nature of Business Premises: Whether the business premises is owned or rented can also play a role in the decision-making process.

Punjab National Bank NRI Personal Loan Eligibility: Requirements for Non-Resident Indians

Here is the Punjab National Bank’s personal loan eligibility criteria for NRIs.

- Residency Status: The applicant must have the status of a Non-Resident Indian or a Person of Indian Origin (PIO).

- Duration of Stay Abroad: PNB might require the applicant to have stayed abroad for a minimum number of years or have a certain duration of employment in the foreign country.

- Valid Passport & Visa: NRIs need to furnish their valid passports as proof of their NRI status. Additionally, a valid work visa or resident visa of the country of residence may be required.

- Income Source & Stability: The bank will consider the nature of your employment abroad, whether you are salaried or self-employed, and the stability of your income. Documented proof of a stable income, such as payslips or income statements, is essential.

- Minimum Monthly/Annual Income: There could be a specified minimum monthly or annual income requirement, depending on the country of residence and currency strength.

- Overseas Bank Account Statements: PNB will likely ask for bank statements from your overseas bank account to assess your financial health and cash flow.

- Indian Bank Account: Having an NRE (Non-Resident External) or NRO (Non-Resident Ordinary) account with PNB or any other bank in India might be a prerequisite.

- Credit Score: While your Indian credit score might not be as relevant, PNB may consider a credit report from the country of your residence to assess your creditworthiness.

- Age Criteria: Just like with resident loans, there’s likely to be an age bracket within which the applicant should fall to be eligible.

- Purpose of Loan: The bank might want to understand the purpose of the loan, especially if it’s related to property or investment in India.

Special PNB Personal Loan Eligibility for Women Applicants

Punjab National Bank recognises the imperative role of women in the socio-economic landscape and offers specialised personal loan eligibility criteria for female applicants. It offers loans under the PNB Mahila Udyami scheme. Eligible candidates include individual women, women entrepreneurs, or businesses where women have a financial stake of 50% or more. Priority will be accorded to women from ST/SC communities and those with BPL cards. Additionally, women entrepreneurs who have undergone training at R-SETIs, Skill Development Institutions, or similar recognised training centres will be preferred. It’s essential that applicants have a clear record with no defaults at any bank or financial institution. Beneficiaries who have already secured loans under government-sponsored programmes are not qualified for the PNB Mahila Udyami initiative.

List of Factors Affecting PNB Personal Loan Eligibility

Here is the list of factors that affect PNB Personal Loan eligibility:

- Credit Score: A good credit score indicates creditworthiness and a history of timely repayments, making it a significant factor in the decision-making process.

- Age: Applicants generally need to fall within a specified age bracket, which may differ for salaried and self-employed individuals.

- Monthly/Annual Income: A steady income ensures that the borrower can meet the monthly repayment commitments. The bank might set minimum income criteria based on the applicant’s profile.

- Employment Stability: The duration an applicant has been employed with their current employer or the stability of a self-employed individual’s business can influence eligibility.

- Debt-to-Income Ratio: The proportion of one’s income used to service existing debts. A lower ratio indicates higher repayment capability.

- Nature of Employment: Permanent employees may have an advantage over contractual or temporary workers.

- Residential Status: Owning a residence as opposed to renting can sometimes be seen as a sign of stability.

- Business Profitability and Turnover (for Self-Employed): These factors indicate the financial health of a business.

- Purpose of the Loan: The intended use of the loan amount might be evaluated, especially for larger loan amounts.

How can you Improve your PNB Personal Loan Eligibility?

Here’s how you can improve your PNB personal loan eligibility:

- Improve Your Credit Score: To improve your credit score, it is imperative that you pay your existing loan and credit card bills on time. Also, make sure that you clear any outstanding dues, even if they are small amounts. It is also important to not apply for multiple loans or credit cards simultaneously.

- Maintain Stable Employment: Lenders, whether be banking or non-banking institutions, always prefer borrowers with stable jobs. Being in the same job for a longer period of time can reflect stability.

- Increase Income: A higher income can boost your loan eligibility as it improves your overall repayment capability. Also, regularly updating your income records with the bank can prove to be helpful here.

- Apply with a Co-applicant: One of the best ways to improve your PNB personal loan eligibility is to combine your income with that of a spouse or family member. It can help you increase your personal loan eligibility amount.

- Choose a Longer Tenure: Opting for a longer loan repayment option might help you reduce the monthly EMIs, making the loan more manageable. Opting for a longer loan repayment tenure might reduce the monthly EMI, making the loan more manageable. Each loan application involves a credit check, and multiple checks in a short span can negatively impact your credit score.

- Maintain a Good Banking Relationship: Having a long-term and positive relationship with PNB can work in your favour. Having a long-term, positive relationship with PNB (or any bank) can work in your favour. This includes maintaining a good average monthly balance and avoiding cheque bounces.

Understanding Impact of Credit Score on Punjab National Bank Personal Loan Eligibility

A credit score, often generated by credit bureaus like CIBIL in India, is a three-digit numerical representation of an individual’s creditworthiness. It plays a pivotal role in determining the eligibility for personal loans, including those from Punjab National Bank (PNB). Here’s how your credit score can impact your personal loan eligibility with PNB:

- Individuals with higher credit score may get loans at more competitive interest rates.

- A good credit score can potentially lead to approval for a higher loan amount.

- A robust credit score can also offer more flexibility in choosing a longer repayment period.

- Based on the credit score, the bank might set additional terms, such as requiring a co-signer or any additional documentation.

- A strong credit score can provide applicants with better negotiation power regarding loan terms, interest rates, or other related conditions.

- Banks occasionally roll out special loan offers for individuals with outstanding credit scores, which might include reduced interest rates, waived processing fees, or other benefits.

Comparing Eligibility across Different PNB Personal Loan Products

| Personal Loan Product | Eligibility | Margin | Security | Prepayment Charges | Documentation Charges |

| Personal Loan for LIC Employees | Employees with a minimum of 1 year of experience | Nil | Nil if the salary amount credited to the bank is more than INR 75,000. In other cases, suitable third party guarantee acceptable to the bank | Nil | Nil |

| Personal Loan for Public | All confirmed employees of Central/State/PSUs with 2 years of service | Nil | Suitable third party guarantee acceptable to the Bank | Nil | Up to Rs 2 lakh- Rs 270

Above Rs 2 lakh- 450 For Defence Personals- NIL |

| Personal Loan for Doctors | For meeting expenses of professional/personal requirements | Nil | Suitable third party guarantee acceptable to the Bank

Tangible Collateral Security of the value of 100% of loan amount |

Nil | Rs. 450 |

| Personal Loan for Pensioners | All types of pensioners drawing pension through our branches | Nil | Guarantee of spouse eligible for family pension to be obtained OR guarantee of earning children (preferably Govt. Employee) OR third party guarantee with net means equal or more than loan amount, acceptable to the Bank | Nil | Rs. 500 |

Frequently Asked Questions (FAQs)

How much salary is required to apply for a personal loan at Punjab National Bank?

While Punjab National Bank has certain salary criteria for personal loans, the exact amount may vary based on various factors, including the applicant’s profile, type of employment (salaried or self-employed), and the loan scheme. It’s recommended to check the latest criteria directly with PNB or on their official website.

What is the bare minimum CIBIL score required to apply for a personal loan at PNB?

One needs a CIBIL score of at least 750 and above to apply for a PNB personal loan.

Do I need to be an existing PNB customer to get their loan?

Being an existing PNB customer can help in getting a loan; however, it is not required to be so. PNB offers personal loans to both existing and new applicants.

What kind of income is required to be eligible for a PNB personal loan?

Needless to say, income is an important factor that helps in getting a personal loan approved. However, apart from your personal income, the bank will also factor in other points such as existing liabilities, employment stability, etc.

How can I increase my personal loan eligibility to apply for a PNB personal loan?

The very basic way to increase your personal loan eligibility would be to improve your credit score.

Quick Links

Loan Offers By Punjab National Bank's

Personal Loan Calculators

Punjab National Bank Calculators

Bank wise Personal Loan Calculators

- Axis Bank Personal Loan Calculator

- Canara Bank Personal Loan Calculator

- Idfc First Bank Personal Loan Calculator

- Hsbc Personal Loan Calculator

- Indusind Bank Personal Loan Calculator

- Hdfc Bank Personal Loan Calculator

- Kotak Bank Personal Loan Calculator

- State Bank Of India Personal Loan Calculator

- Idbi Bank Personal Loan Calculator

- Indiabulls Personal Loan Calculator

- Muthoot Finance Ltd Personal Loan Calculator

- Paysense Personal Loan Calculator

- Bajaj Finserv Personal Loan Calculator

- Tata Capital Financial Services Ltd Personal Loan Calculator

- Hero Fincorp Personal Loan Calculator

- Karur Vysya Bank Personal Loan Calculator

- Union Bank Of India Personal Loan Calculator

- Punjab National Bank Personal Loan Calculator

- Bank Of India Personal Loan Calculator

- Bank Of Baroda Personal Loan Calculator

- Punjab Sind Bank Personal Loan Calculator

- Indian Bank Personal Loan Calculator

- Bank Of Maharashtra Personal Loan Calculator

- Citi Bank Personal Loan Calculator

- Rbl Bank Personal Loan Calculator

- Karnataka Bank Personal Loan Calculator

- Federal Bank Personal Loan Calculator

- Deutsche Bank Personal Loan Calculator

- Yes Bank Personal Loan Calculator

- Dcb Bank Personal Loan Calculator

- Icici Bank Personal Loan Calculator